4 Defensive Dividend Stocks That Can Survive a Recession🛡️

Companies That Keep Paying No Matter What the Market Does

Recessions hit hard. Markets fall. Portfolios get shaky. But some companies just keep paying. I know I talk a lot about higher yielding assets, but it’s important to also have a sizeable weight in blue chip dividend growth companies that can provide stability and reliable income through market uncertainty.

As a dividend investor, I don’t just want income. I want reliable income. I want the kind that keeps coming in whether the economy is booming or slowing down. Whether markets go up, down, or sideways, I still want to continue to collect dividends throughout.

That’s why I build part of my portfolio around defensive dividend stocks. These are companies that sell things people buy no matter what; toothpaste, food, coffee, cigarettes, soap, and all the essentials. Their cash flows hold up in a downturn, and their dividends usually keep growing.

Here are four defensive dividend stocks I own or closely watch when I want income that can survive a storm.

What Makes a Dividend Grower Worth Owning?

Not all dividends are created equal. A high yield might look appealing, but experienced investors understand that the reliability and sustainability of a dividend matter more than the headline number.

Here are a few key things to watch for when selecting a quality dividend growth stock:

1. Payout Ratio

The payout ratio measures how much of a company’s earnings are paid out as dividends. For example, if a company earns five dollars per share and pays two dollars and fifty cents in dividends, that is a fifty percent payout ratio.

A moderate payout ratio, typically between thirty and sixty percent depending on the industry, indicates a balance between rewarding shareholders and retaining profits for future growth. Ratios that are too high can signal that the dividend may be at risk if earnings decline.

2. Dividend Growth Rate

Look for companies that not only pay a dividend but raise it consistently. A healthy dividend growth rate, ideally five percent or higher per year, helps protect your income against inflation and increases your cash flow over time.

The longer the dividend growth streak, the more confidence you can have in the company’s commitment to its shareholders.

3. Free Cash Flow

Cash flow is the lifeblood of any dividend strategy. Even if earnings look strong on paper, what matters is how much actual cash the company generates after expenses. That is what funds the dividend.

Companies that consistently produce strong free cash flow are in a better position to maintain and grow their payouts through all market conditions.

4. Financial Strength

Check the balance sheet. Companies with low debt levels and strong interest coverage are better equipped to handle economic stress while continuing to reward shareholders.

Financial discipline is a good sign that management takes long-term performance seriously.

5. Business Stability

Some industries are naturally more resilient. Sectors like consumer staples, utilities, and healthcare tend to hold up better when the economy slows down.

Businesses that sell everyday products or essential services often have more predictable revenue, which supports reliable dividend payments over time.

🧼 1. Procter & Gamble (PG)

Dividend Yield: ~2.5%

Payout History: 68 consecutive years of dividend increases

Sector: Consumer Staples

Procter & Gamble is a dividend fortress. It owns brands you use every single day: Tide, Crest, Gillette, Dawn, Pampers, and more. When people tighten their budgets, they still buy soap, toothpaste, and diapers. That’s why PG is one of the most recession-resistant stocks on the planet.

It’s also a Dividend King, with more than six decades of consecutive dividend hikes. The company generates strong free cash flow, maintains a conservative payout ratio, and has pricing power even during inflation.

PG isn’t a high-yield play. But it’s about as stable as it gets. I accumulated $10,000 worth of PG back in 2020 and continue to hold today.

🛒 2. Kroger (KR)

Dividend Yield: ~2%

Payout History: 18 consecutive years of increases

Sector: Grocery / Retail

You’ll notice how low KR’s payout ratio is.

Kroger runs one of the largest grocery chains in the U.S. And when the economy turns south, people don’t stop eating. They often stop eating out.

That makes grocery chains a recession-resistant business and Kroger is among the best managed in the space. Its low payout ratio, steady buybacks, and improving margins make it a quietly powerful income stock.

Kroger won’t explode to the upside, but in a downturn, it tends to hold the line, all while continuing to pay and raise its dividend.

There is one reason why I am so optimistic on Kroger’s future success:

One of the most overlooked strengths behind Kroger’s stability is its powerhouse portfolio of private label brands. These are store brands like Simple Truth, Private Selection, and Home Chef that are owned and developed by Kroger itself.

Private labels matter for two key reasons. First, they offer higher margins than national brands because Kroger controls production and pricing. That improves profitability even when overall sales are flat. Second, they build customer loyalty. Many shoppers seek out Kroger’s private label products specifically for their value, quality, and consistency.

During inflationary periods or economic slowdowns, consumers often trade down from premium brands to store brands. That shift actually benefits Kroger. Its private labels generate over thirty billion dollars in annual sales and continue to grow as more customers prioritize value.

This private label dominance gives Kroger a built-in cushion during downturns. It supports earnings, protects margins, and helps the company maintain a steady stream of cash flow to keep raising its dividend. In other words, it is one of the quiet strengths that makes Kroger a reliable income stock for long-term investors.

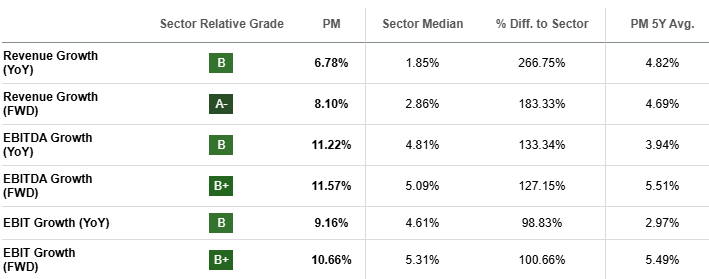

🚬 3. Philip Morris International (PM)

Dividend Yield: ~3%

Payout History: 16 years - Consistent annual increases since its 2008 spinoff from Altria

Sector: Tobacco

Whether you love or hate the industry, Philip Morris has proven to be one of the most reliable dividend payers out there.

It owns the Marlboro brand internationally, along with newer reduced-risk products like IQOS, which is gaining ground in many global markets. The business is highly cash generative and has limited economic sensitivity since people don’t typically quit smoking because of a recession.

PM is not just a high yielder. It’s a cash-flow machine with pricing power, a global footprint, and a management team committed to returning capital to shareholders.

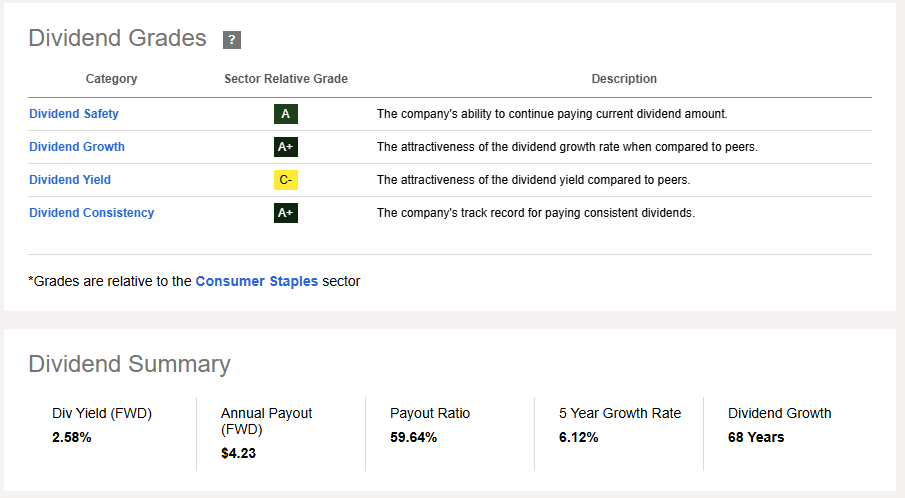

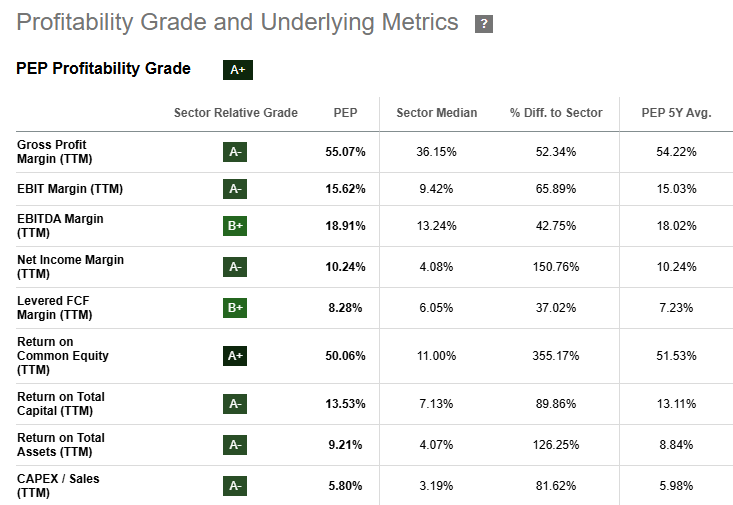

🥤 4. PepsiCo (PEP)

Dividend Yield: ~4.3%

Payout History: 52 consecutive years of increases

Sector: Beverages and Snacks

PepsiCo is more than soda. It owns Frito-Lay, Gatorade, Tropicana, Quaker, and Doritos, which gives it powerful diversification across both beverages and food. Pepsi has fallen by about 25% over the last twelve months but I believe this offers an attractive opportunity to begin accumulating shares.

That matters in a downturn. Even when consumers cut back, they still buy snacks and drinks. Pepsi’s scale and global reach allow it to pass on rising costs without damaging demand.

Pepsi is also a Dividend King, having raised its dividend for over 50 years in a row. It’s not flashy, but it’s rock solid and the dividend is backed by strong fundamentals and recession-tested brands. Despite the shortcomings and decline due to higher inflation, shifts in consumer spending, and uncertainty around tariffs, Pepsi remains highly profitable.

I currently own $12k worth of Pepsi and will be looking to add another $8k to my position here at these levels.

✅ Final Thoughts

Building an income portfolio isn’t just about chasing yield. It’s about survivability. If your dividends vanish in a recession, the strategy falls apart.

That’s why I keep a defensive layer in my portfolio — reliable names with decades of dividend history, pricing power, and products people always need.

PG. KR. PM. PEP. These companies have paid through inflation, war, and economic downturns. And they’re still paying.

If you're looking to fortify your income stream, these four are a great place to start.