Build Your Own Rental Empire With These 4 REITs

Collect Steady Income Like a Landlord Without Ever Buying A Physical Property

Imagine collecting rent checks every month from prime shopping centers, luxury casinos, grocery anchored retail strips, and iconic office buildings without ever buying a single property or managing a single tenant.

No down payments. No mortgages. No late night phone calls.

Just steady, passive income flowing into your account.

For years, building a real estate portfolio meant jumping through hoops. You had to save for a huge down payment, take on debt, manage property repairs, and deal with all the stress that comes with being a landlord. Even REITs, once considered niche investments, were often overlooked by dividend investors in search of bigger and faster returns.

But that is changing. Fast.

Today’s market has given income investors a unique opportunity. Several Real Estate Investment Trusts are trading at discounted valuations, offering higher yields and better long term upside than we have seen in years. These are professionally managed portfolios of income generating properties, packaged into a liquid stock you can buy with a single click.

REITs let you own the cash flow of real estate without owning the real estate itself. And for investors looking to build a scalable, stress free income stream, that is a game changer.

Why Collecting Rent From REITs Just Makes Sense

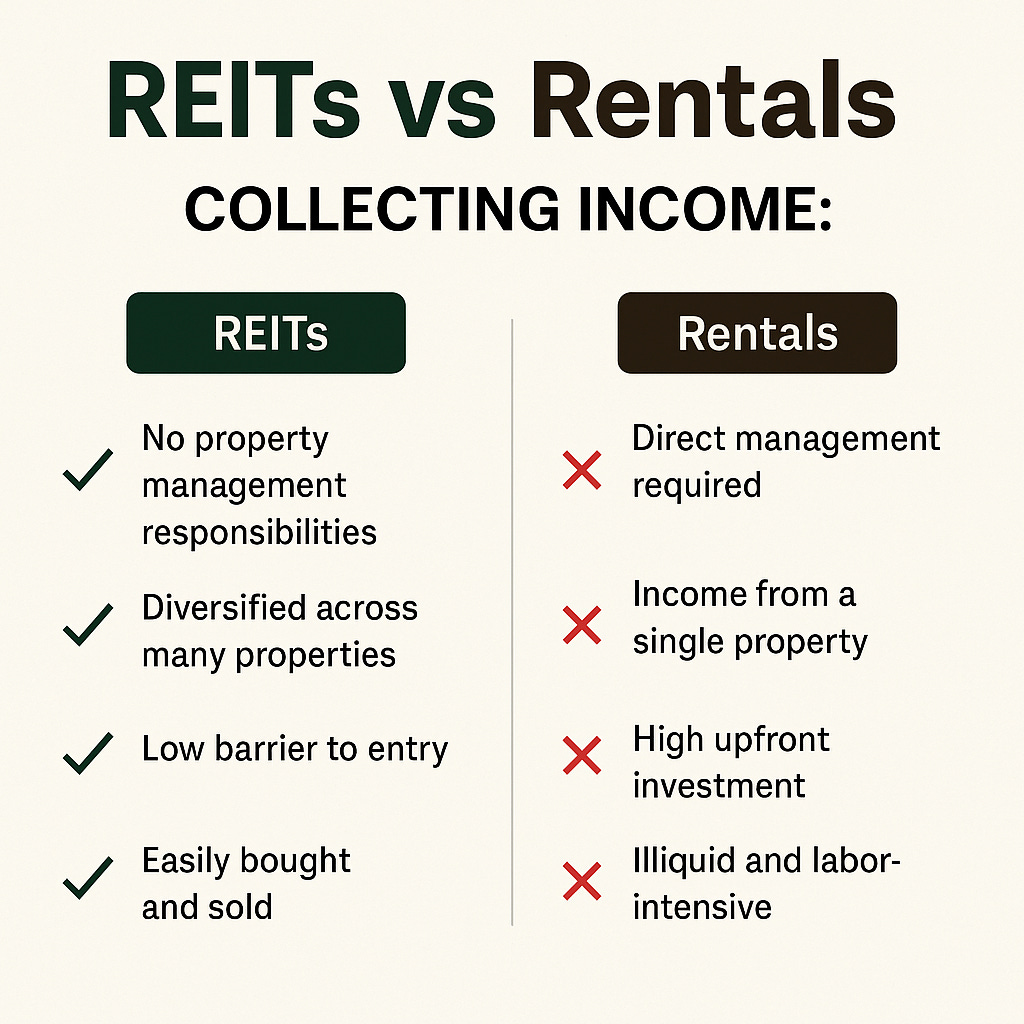

Collecting income from REITs offers all the benefits of real estate investing without the barriers, the headaches, or the risk of going it alone. Whether you are a retiree looking for stable cash flow or a younger investor building a passive income stream over time, REITs provide a practical and scalable path to consistent payouts.

One of the most important benefits is accessibility. With REITs, you do not need a six figure down payment or a high credit score to become a landlord. You can buy shares of professionally managed real estate portfolios with just a few hundred dollars and receive distributions just like any property owner would. This levels the playing field for investors who want exposure to real estate but prefer the simplicity and liquidity of the stock market.

Then there is the diversification factor. Owning a single rental property comes with concentrated risk. If your tenant moves out, your income stops. If repairs pop up, your cash flow disappears. With REITs, your income comes from hundreds, even thousands of tenants spread across geographic regions, industries, and property types. That diversification helps smooth out volatility and adds resilience to your portfolio.

Another major advantage is tax efficiency. While REIT dividends are taxed as ordinary income, many REITs also return capital through depreciation benefits and capital structure strategies that can reduce your tax burden or defer it altogether. And if held in a tax advantaged account like a Roth IRA, those distributions can compound completely tax free.

There is also zero operational burden. You do not have to screen tenants, manage properties, deal with contractors, or chase rent checks. The REIT’s management team handles everything. Your only job is to decide how much exposure you want, collect the income, and decide whether to reinvest or spend it.

Finally, REITs offer the unique advantage of liquidity. Unlike physical real estate, you can buy or sell shares of a REIT instantly through your brokerage account. That means greater flexibility and control over your income strategy—something traditional landlords simply do not have.

When you step back, collecting income from REITs allows you to experience the upside of real estate ownership without the common pitfalls. You get consistent income, professional management, exposure to appreciating assets, and the freedom to scale your portfolio on your own terms.

Simon Property Group (SPG)

Sector: Retail Malls

Dividend Yield: 5%

Dividend Schedule: Quarterly

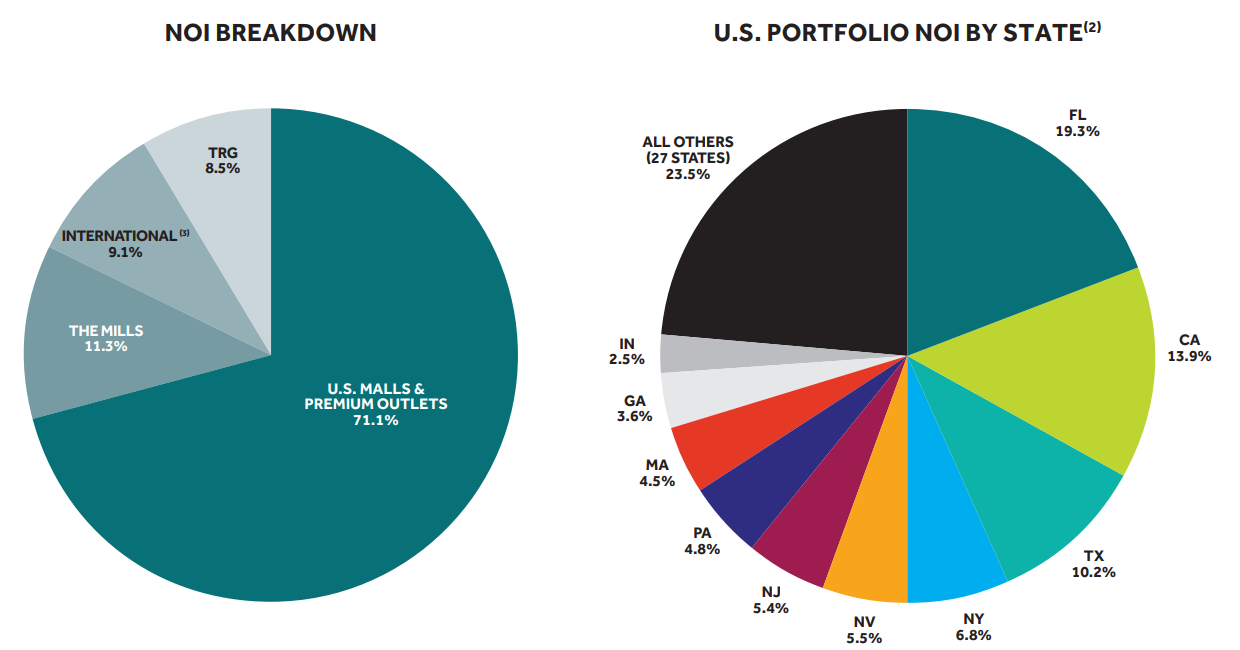

Simon Property Group is not your average mall operator. It is the largest retail real estate investment trust in the world, with ownership in some of the most prestigious and high performing shopping centers across the United States and internationally. This includes Class A malls, premium outlets, and mixed use lifestyle centers that are strategically located in high traffic, high income areas.

While some investors remain skeptical about the future of malls, SPG has been proving them wrong. The company is not focused on dying suburban retail. Instead, it has leaned heavily into repositioning and upgrading its properties with restaurants, entertainment venues, co working spaces, and even residential units. In many cases, Simon is transforming traditional retail properties into modern, multi use experiences that are far more resilient in a post pandemic economy.

Financially, SPG is as solid as they come in the REIT world. The company generates billions in funds from operations and maintains strong liquidity with a well managed debt profile. They are also shareholder focused, consistently returning capital through dividends and buybacks. In fact, SPG has been aggressively increasing its dividend payout since slashing it during COVID, and the current yield sits around 5.6 percent with further upside potential.

What makes SPG especially interesting for long term income investors is that it blends yield with quality. You are not just getting a high dividend—you are getting a stake in prime real estate backed by strong tenant demand and professional management. This is one of the few retail REITs that has both size and scale, and its performance over the past decade reflects that leadership.

While sentiment around retail real estate may fluctuate, Simon Property Group continues to quietly dominate its space and reward patient investors who look past the headlines. It is a cornerstone holding in my REIT portfolio and one of the best ways to collect reliable income from retail without needing to bet on every individual tenant.

Agree Realty (ADC)

Sector: Net Lease Retail

Dividend Yield: 4.1%

Dividend Schedule: Monthly

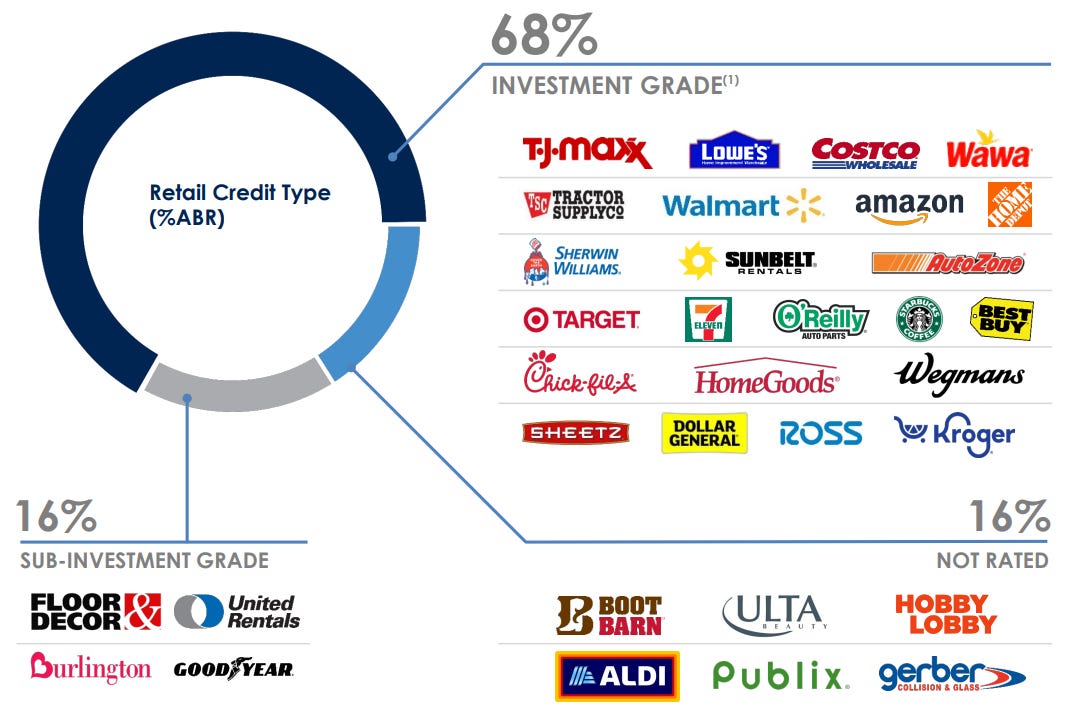

Agree Realty is one of the most reliable income generators in the real estate space today. It specializes in single tenant, net lease retail properties leased to some of the most recession resistant businesses in America. Think companies like Walmart, Tractor Supply, Dollar General, AutoZone, and Walgreens. These are the types of tenants that continue operating even during economic downturns, which provides a level of consistency that dividend investors can depend on.

What makes Agree Realty especially appealing is its triple net lease model. In this structure, tenants are responsible for paying taxes, maintenance, and insurance, which reduces costs and operational headaches for the landlord. This results in very predictable income streams and highly stable cash flow, even in a volatile market. For long term income investors, this predictability is invaluable.

Unlike many REITs that pay dividends quarterly, ADC pays investors every single month. That monthly cadence creates a smoother income stream that feels more like a paycheck and is ideal for retirees or anyone looking to build consistent cash flow. The company has also delivered steady dividend growth, with increases nearly every year since going public.

Agree Realty is also extremely conservative in how it manages its business. Its balance sheet is strong, with investment grade credit ratings and a history of disciplined growth. The management team has consistently executed on smart acquisitions and strategic developments that enhance shareholder value without overleveraging the company.

In terms of portfolio composition, ADC owns more than two thousand properties across forty nine states, covering a wide variety of essential retail categories. This geographic and tenant diversification helps protect against localized downturns or disruptions in specific industries. Even as trends shift in the broader economy, people still need pharmacies, convenience stores, and discount retailers—all areas where Agree Realty has strong exposure.

In short, ADC is a no drama REIT. It does not swing for the fences, but it hits singles every month and piles up steady returns year after year. If your goal is to collect consistent, inflation beating income from a high quality real estate portfolio, Agree Realty should absolutely be on your radar.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

🧠Starter Kit

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

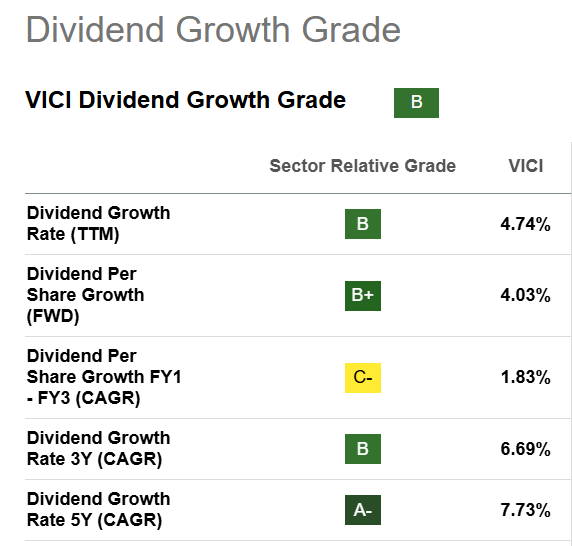

VICI Properties (VICI)

Sector: Gaming and Hospitality

Dividend Yield: ~5.4%

Dividend Schedule: Quarterly

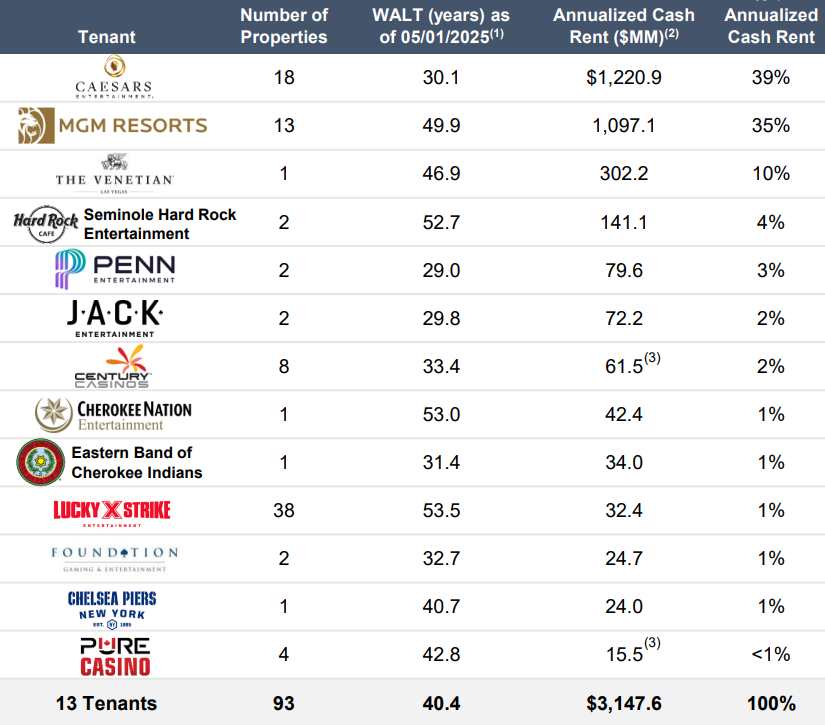

VICI Properties is one of the most fascinating REITs in the market today. It offers investors the opportunity to collect rent from some of the most iconic entertainment assets in the world, including Caesars Palace, MGM Grand, the Venetian, and dozens of other high profile casino and hospitality properties across the United States.

But here is what makes VICI so attractive. The company does not actually run the casinos. It owns the physical real estate and leases it out to highly experienced operators through long term contracts. These leases are typically structured as triple net agreements, meaning the tenants are responsible for property expenses such as maintenance, taxes, and insurance. That allows VICI to generate extremely reliable cash flows with very little operational risk.

Most of VICI’s leases are not only long term but also inflation linked. That means rent payments automatically increase over time, protecting your income stream from the erosion of purchasing power. In fact, many of VICI’s lease agreements span decades and include built in escalators that ensure rising rent regardless of short term economic noise.

Since its spin off from Caesars Entertainment in 2017, VICI has aggressively grown through acquisitions, establishing itself as the dominant player in the gaming real estate space. It has built an enviable portfolio in a niche sector with high barriers to entry and few competitors. And the growth story is far from over. VICI has recently expanded into new categories like experiential real estate and international assets, giving it even more room to scale its income engine.

What is especially compelling about VICI is the combination of high yield, long term visibility, and relatively low volatility. Despite operating in a flashy industry, the company itself is quite stable thanks to its focus on contractual cash flows and conservative financing. It has investment grade credit ratings and maintains a strong balance sheet that supports continued dividend growth.

For investors who want exposure to real estate with strong cash flow and inflation protection, VICI offers a powerful solution. It is a great example of how REITs can tap into unconventional income streams in a very tax efficient and scalable way. Whether or not you are a fan of Vegas, owning VICI lets you collect rent from the Strip and beyond, all while sitting comfortably at home.

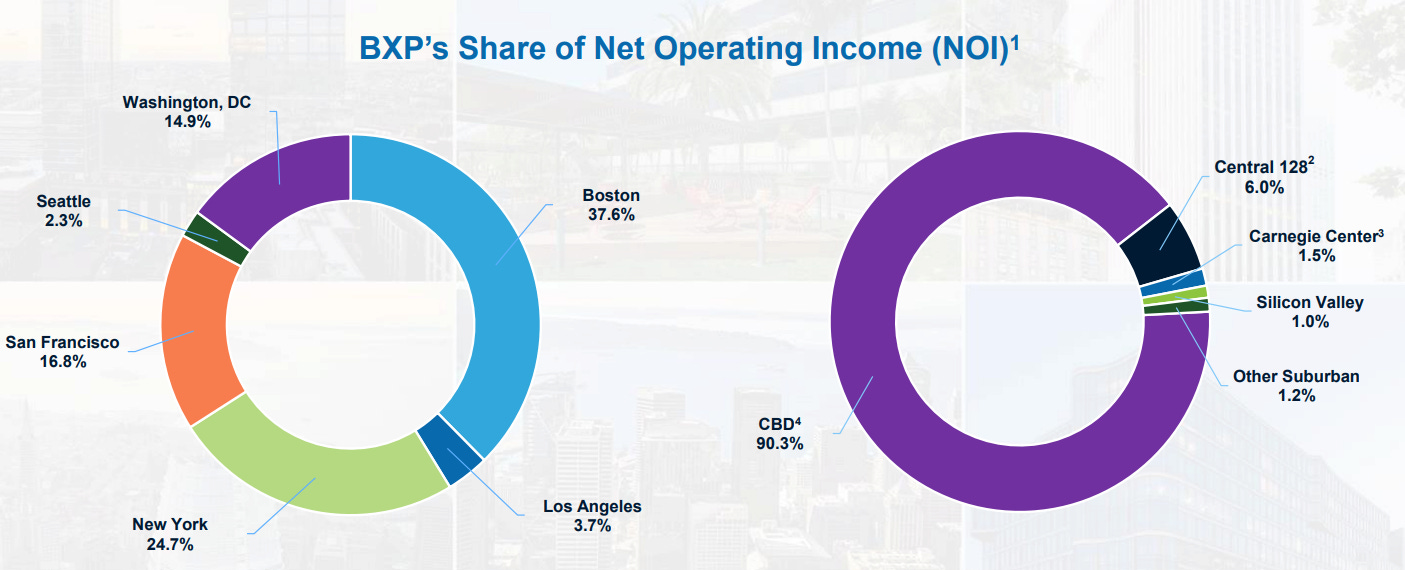

Boston Properties (BXP)

Sector: Office

Dividend Yield: 5.8%

Dividend Schedule: Quarterly

Boston Properties is one of the largest and most respected owners of Class A office buildings in the United States. With a portfolio spanning more than fifty million square feet of premium office space, BXP focuses on high demand urban markets such as Boston, New York City, San Francisco, Washington D.C., and Los Angeles. These are markets where supply is limited, tenant quality is high, and long term demand for top tier office space tends to hold firm—even in periods of economic uncertainty.

Let us be honest. Office REITs are unloved right now. The work from home movement has created real disruption in commercial real estate, and many investors have written off the entire sector. But that broad brush ignores an important distinction. Not all office space is equal. Boston Properties does not lease out dated buildings in declining suburbs. It focuses exclusively on institutional grade, highly amenitized, environmentally sustainable office towers that serve the Fortune 500, global law firms, tech companies, and government tenants.

And even amid the challenges facing the sector, BXP has held its ground. Occupancy remains strong across its core properties, lease renewal rates are stable, and the company continues to collect the overwhelming majority of its rent. At the same time, BXP has taken proactive steps to reposition its portfolio for the future. This includes investing in flexible workspace layouts, mixed use developments, and innovation campuses that meet the changing demands of hybrid workforces.

What makes Boston Properties particularly interesting for income investors is its current valuation and yield. With the stock trading at a deep discount to net asset value, the dividend yield sits at approximately 6.1 percent, which is unusually high for a REIT of this quality. The company has also taken a disciplined approach to capital management, balancing shareholder returns with debt reduction and development opportunities.

In many ways, BXP represents a classic contrarian opportunity. When a high quality company trades at depressed prices due to short term industry headwinds, it can create a rare setup for long term investors who are willing to look beyond the headlines. If and when sentiment toward office space begins to normalize, Boston Properties could see both price appreciation and continued income growth.

Even if the recovery takes time, BXP’s strong balance sheet, conservative leadership, and premium real estate holdings make it a compelling option for those seeking reliable dividends from a deeply discounted asset. It is not for the risk averse, but for those willing to be patient, the reward potential is substantial

Conclusion: Build Income the Smarter Way

You do not need to buy rental properties to build a steady stream of income. You do not need tenants, toilets, or a six-figure down payment. With the right REITs, you can collect rent checks backed by high-quality real estate—right from your brokerage account.

Whether you are looking for monthly cash flow, inflation protection, or exposure to income-producing assets without the operational burden, REITs offer a powerful solution. SPG gives you premium mall exposure, ADC delivers essential retail income on a monthly basis, VICI taps into the cash flow of iconic casinos, and BXP offers contrarian upside in elite office properties. Together, these REITs form a diversified foundation for a passive income strategy rooted in real estate fundamentals.

You are not just buying stocks. You are building a rental empire without the complexity—and getting paid to hold.