Starbucks: Why This Dividend Stock Is Undervalued

Potential 18% Upside & Brewing a New Chapter Under Fresh Leadership

Overview

If you listen to coffee critics, you might think Starbucks' days are numbered. Overpriced coffee, overpriced brand, easy to replicate at home. But take one look at real-world locations, and the truth is obvious: Starbucks remains a cultural phenomenon. Lines at the drive-thru, packed tables inside, people willing to wait 20 minutes just for that familiar cup.

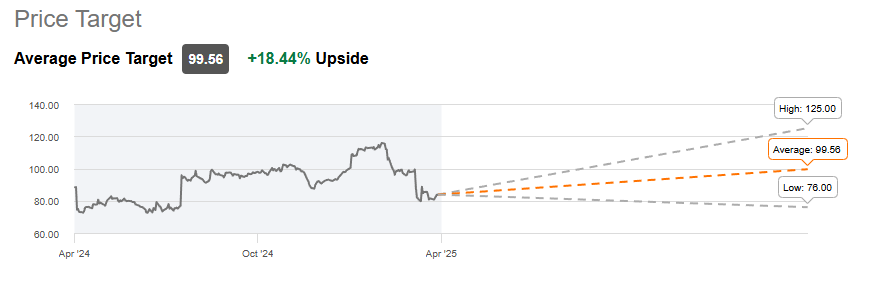

Leadership recently shifted within Starbucks and management has made it clear that they are aiming for better operational efficiency and quality of life improvements. With an average price target f $99.56 per share, this indicates a potential upside of 18.4% from the current price level.

Operational Shifts

The new leadership wasted no time in making meaningful changes.

First, Starbucks began closing underperforming locations, trimming operations that were dragging down overall efficiency. In addition, the company announced layoffs of approximately 1,100 corporate employees. While painful, these moves are essential for streamlining the organization and re-focusing capital where it generates the highest return.

Niccol also ended generous remote work policies, requiring corporate leaders to be in the office at least three days a week. A tighter, more engaged leadership team is crucial for a service-driven business like Starbucks.

At the store level, the goal is simple: increase foot traffic and encourage customers to stay longer. Starbucks introduced changes including:

Condiment bars for easier personalization

Free refills for customers staying in the cafes

Simplified menus

More comfortable seating areas

Targeted marketing campaigns

Within less than 12 months, these small tweaks have led to a 300 percent increase in the number of customers choosing to stay inside U.S. locations.

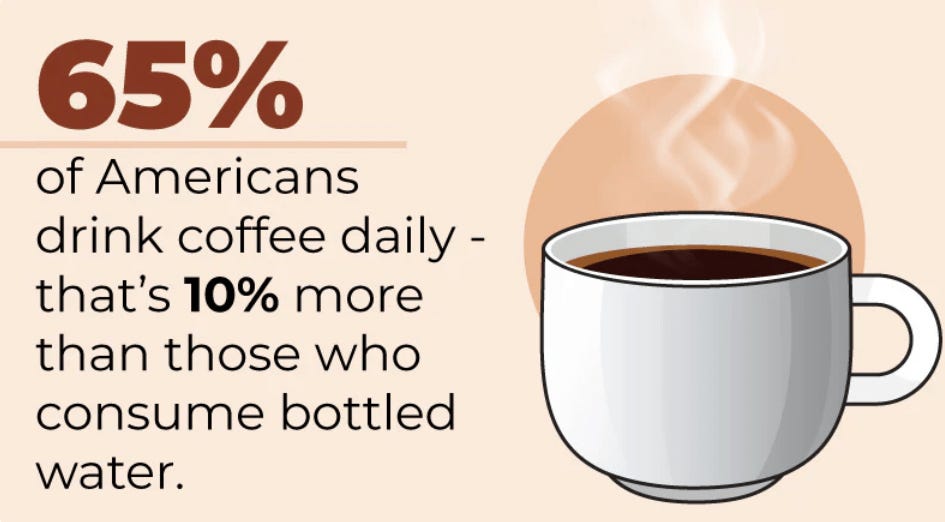

These operational shifts are tapping into something deeper than just caffeine. Coffee holds emotional and cultural significance in America. Statistics show that coffee consumption has hit a 20-year high, outpacing bottled water in daily consumption rates. Starbucks is selling more than coffee — it is selling a ritual, a habit, and a small moment of pleasure.

Critics who argue that customers will "wake up" and start making coffee at home misunderstand the power of branding, loyalty, and emotional connection. The same logic could be applied to why people continue to buy iPhones or luxury cars despite cheaper alternatives. Human psychology, not rationality, drives consumption.

If Starbucks can continue leaning into this emotional attachment while improving in-store experience, customer traffic will only strengthen — particularly as we move into the historically stronger July through November growth season.

Financials and Valuation

Financially, Starbucks remains in a solid position but is not without vulnerabilities.

Cash and equivalents rose to $3.67 billion this past quarter, up from $3.28 billion, providing a healthy liquidity cushion. However, long-term debt has grown significantly in recent years, now totaling $14.3 billion. In a higher interest rate environment, this debt load carries more risk, as interest expenses climb alongside rates.

Currently, Starbucks pays out $549.1 million annually in interest expenses, near the highest level seen over the last decade. Management has yet to signal an aggressive debt reduction plan, which is something I will be monitoring closely throughout 2025.

Despite the debt burden, operational performance is improving. In the most recent Q1 earnings:

EPS came in at $0.69, beating estimates by $0.02

Revenue reached $9.4 billion, beating by $90 million

Comparable global sales fell 4 percent, though the decline moderated compared to prior quarters

The modest drop in comps should not be overemphasized. Given the operational reset underway, stabilizing results are a positive sign. Notably, the Starbucks Rewards loyalty program grew by 1 percent year-over-year, suggesting customer engagement remains intact.

Profitability metrics remain strong:

EBITDA margin: 17.75% (sector median: 11.75%)

Net income margin: 9.73% (sector median: 4.52%)

Free cash flow per share: $2.57, back to pre-pandemic levels

From a valuation perspective, Starbucks trades at a forward P/E ratio of 33x, compared to a sector median of 16x. On paper, this looks expensive. However, Starbucks’ global scale, brand loyalty, and upside from operational improvements justify a premium multiple.

Wall Street's average price target sits at $107.51 per share, offering around 10 percent upside from current levels. Higher-end targets reach $125, and with a strong operational turnaround underway, I would not be surprised to see Starbucks retesting higher valuations within the next year.

Income Machine

One of Starbucks’ most attractive features for long-term investors remains its dividend.

The company announced a 7 percent dividend increase, bringing the quarterly payout to $0.61 per share and a forward yield of about 2.5 percent. Starbucks has now raised its dividend for 14 consecutive years, with a stellar 15 percent CAGR over the last decade. However, investors must pay attention to the rising payout ratio. With comps softening and earnings growth slowing temporarily, Starbucks’ payout ratio now exceeds 76 percent. While this is an improvement over the prior five-year average of 94 percent, it remains elevated compared to the sector median near 35 percent.

Given the company's focus on operational efficiencies and cash flow generation, I believe the dividend remains safe in the near term. But longer-term dividend growth will require improving margins and, ideally, some debt reduction.

For long-term holders, patience could be richly rewarded. A yield-on-cost of nearly 4 percent for those who bought five years ago demonstrates the power of consistent dividend growth. Moreover, Starbucks dividends qualify as qualified dividends, offering favorable tax treatment compared to ordinary income.

Vulnerabilities

Starbucks still faces some significant risks.

The first is consumer spending. Inflation remains sticky, and households continue to feel pressure from higher costs across food, housing, and transportation. Coffee is a small luxury, but in tighter budgets, even small luxuries can face pressure.

As inflation cools and wage growth stabilizes, Starbucks could see improving trends. However, any sustained weakness in discretionary spending could weigh on near-term results.

The second major risk is debt.

Higher interest rates are already increasing Starbucks’ financial obligations, and failure to address the debt load could erode future earnings and limit dividend growth. Management has not laid out a clear debt reduction strategy yet, which remains a critical area to watch.

Takeaway

In conclusion, Starbucks is brewing a slow but steady comeback.

Under Brian Niccol’s leadership, operational improvements are taking root. Customer traffic is rebounding. The emotional connection between consumers and the Starbucks brand remains as strong as ever. Coffee demand across the United States is at a 20-year high, giving SBUX a powerful secular tailwind.

While elevated debt levels and inflationary risks require monitoring, the company’s balance sheet, profitability, and strategic repositioning efforts position it well for future growth.

🎁 Free Downloads to Get You Started

These are the two best resources for getting familiar with monthly payers and dividend growth stocks.

✅ 50+ Monthly Dividend Payers List

A curated list of high-yield stocks and funds that pay monthly, perfect for building a ladder of recurring income.✅ Dividend Growth Legends: 50+ Stocks with 25+ Years of Raises

The most consistent dividend companies on the planet—some have increased payouts for over 60 straight years.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

🧠Starter Kit

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters