Target's Stock Trades At A Massive Discount

I plan to invest $10,000 into Target over the next quarter.

Market selloffs can be seen as a blessing. While other investors may panic, long term investors know that these conditions are when wealth is built. Target has fallen by more than 37% over the last twelve months. I think this presents an attractive buying opportunity and I plan to accumulate $10,000 worth of shares over the next quarter.

According to the average Wall St. price targets, TGT has a fair value of about $136.47 per share, indicating a possible upside of 30.48% from the current price level. From a valuation perspective, the stock trades at a price to earnings ratio of 11.55x. In comparison, the consumer sector trades at a median price to earnings ratio of 16.26x, reinforcing the idea that TGT is undervalued. In the best case scenario, analysts estimate that shares can rise as high as $160 per share.

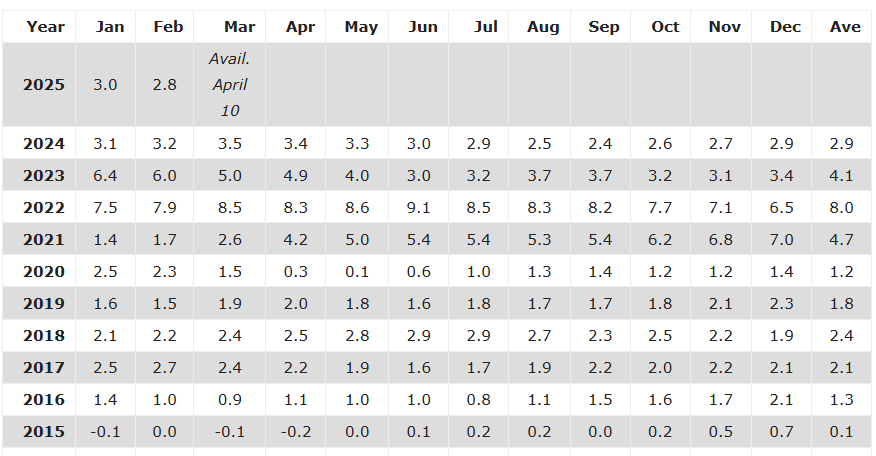

Markets have deemed consumer facing businesses like Target & Walmart unfavorable because of Trump’s ongoing tariff drama that’s caused a trade war, higher than expected inflation rates, a higher interest rate environment, and growing unemployment numbers. These all translate to lower consumer spending activity and it has investors spooked on the outlook of these businesses. Looking at the last earnings report, Target saw very unimpressive growth. 1.5% increase in comparable sales, a modest 2.1% increase in foot traffic, and a 8.7% increase in digital sales. These low single-digit growth rates just aren’t enough to get folks excited nowadays. However, I think the market has overreacted to these results. Although growth has slowed, Target is still growing.

The business is still allocating capital towards different growth initiatives that can drive revenues, earnings, and valuations higher over time. Target committed $3B towards different investments that can drive growth. The business has over $4.7B in cash available at their disposal so Target is well positioned to survive these short term headwinds. Similarly, Target decreased their debt over the last two years and it now sits at $12.2B. See the list of investments below:

What I want to zone in on is the new supply chain facilities that they’ve opened. Target has a wide variety of brands that they own, which can compete with national brand names. Target’s offering is usually more affordable, which means that their products are more likely to see a rising amount of sales as consumers shift their spending habits. Inflation rates continue to be higher than they’ve historically been over the last decade.

A rising cost of goods leads most folk to start considering alternative product choices in the groceries. Instead of buying that Tide laundry soap, you might opt for the store brand soap to save a few dollars. Instead of the brand name toilet cleaner, you might grab the generic brand. Instead of Tylenol, you might grab the Target brand. This concept can be applied to every single sub-category within the consumer space and Target’s ability to distribute their own goods at a more efficient cost, makes them highly competitive.

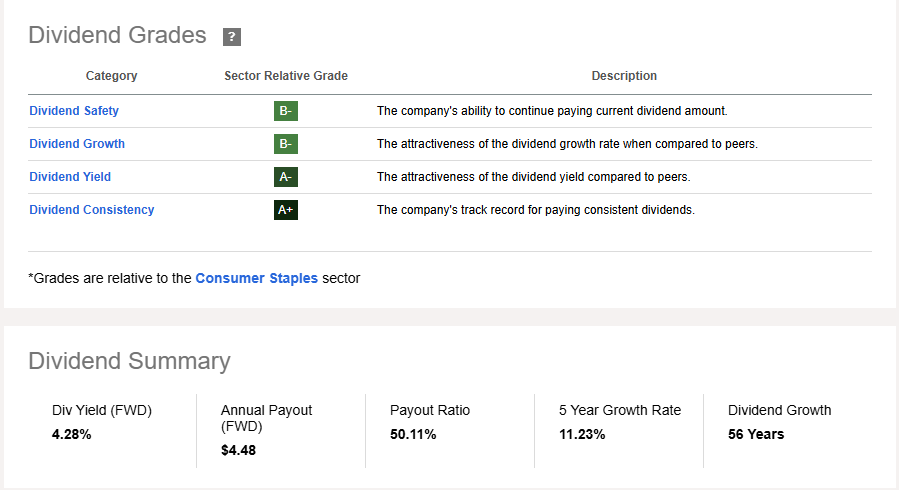

The strong brand competition and strong balance sheet also means that Target can maintain its reputation for consistent dividend increases. The dividend yield currently sits above 4.2% following the price drop. Target has raised its dividend for investors for 56 consecutive years without disruption, effectively earnings the company the title of a ‘Dividend King’. Over the last 5 years, Target has raised dividends at an average annual rate of 11.23%. Have you received a double digit raise this often from your lame ass job? Most people haven’t. Therefore, Target is a great long term choice for long term, tax-efficient income. The dividends are classified as qualified, meaning that you would owe no taxes on these.

Ultimately, the price has declined due to external weaknesses. Consumer traffic may have slowed and the business is delivering slower growth, but this is expected right now. This is a clear window of opportunity to accumulate shares while everyone else is chasing the latest tech stock. We have the opportunity to accumulate shares in a high quality company that will continue delivering a growing source of passive income.

This is just a quick bullet-point type of analysis.

I publish more in-depth analyses like this on a daily basis over on Seeking Alpha. Membership is free. Thanks for reading!

Interesting. I thought Target was last amongst the group of Wmt, Cost etc. seems like they were lagging?