The Financial Sector Will Explode Higher Over The Next Decade

Stablecoins & Cutting Costs. Get Paid A High Yield Of 7.7% While You Wait.

The market is obsessed with who is building the tech. The real wealth transfer, however, is happening within the legacy businesses using that tech to ruthlessly slash costs and print cash.

I call this the age of efficiency. Imagine a business cutting costs to levels once unimaginable. We are already seeing this happen all around us with many of the tech leaders of the world.

Meta Platforms META 0.00%↑ cutting 20% of jobs to save $6B.

Google GOOG 0.00%↑ slashed 35% of managers.

Block XYZ 0.00%↑ cuts 40% of its workforce for efficiency.

Instead of thinking about things logically, people tend to take speculative bets to get rich quick.

The mainstream narrative is telling investors to go buy speculative tech tokens or overvalued software companies to capture this growth (like Palantir PLTR 0.00%↑) . The data suggests a completely different approach.

The greatest wealth transfer of this decade will not go to the companies selling the software. It will go to the established, cash-flowing businesses that are using this new technology to widen their profit margins and massively increase their dividend payouts.

The financial sector is entering a golden age of margin expansion and no one is talking about it. We are going to analyze exactly how financial companies are using Artificial Intelligence and blockchain infrastructure to trigger a profitability boom, and then break down the exact strategy to extract a high-yield income stream from this macro trend.

Get a shortcut on your investing journey with this starter guide. You can get the dividend starter bundle so that you can skip the mistakes that I made on my way to $40,000 a year in passive dividend income.

👉 Here is what’s included:

✅ The Dividend Blueprint (ebook)

A step-by-step guide showing how I structure my portfolio, grow monthly cash flow, and reinvest for long-term income.✅ Monthly Dividend Map

50+ hand-picked tickers that pay monthly so you can ladder your income all year long.✅ Dividend Tracker (Google Sheet)

The exact spreadsheet I use to track yield, forward income, reinvestment, and portfolio growth.✅ Dividend Growth Legends: 50+ Stocks

50 stocks that have an established history of dividend increases.✅ List of ETFs for Beginners To Start With

The AI Cost-Cutting Machine

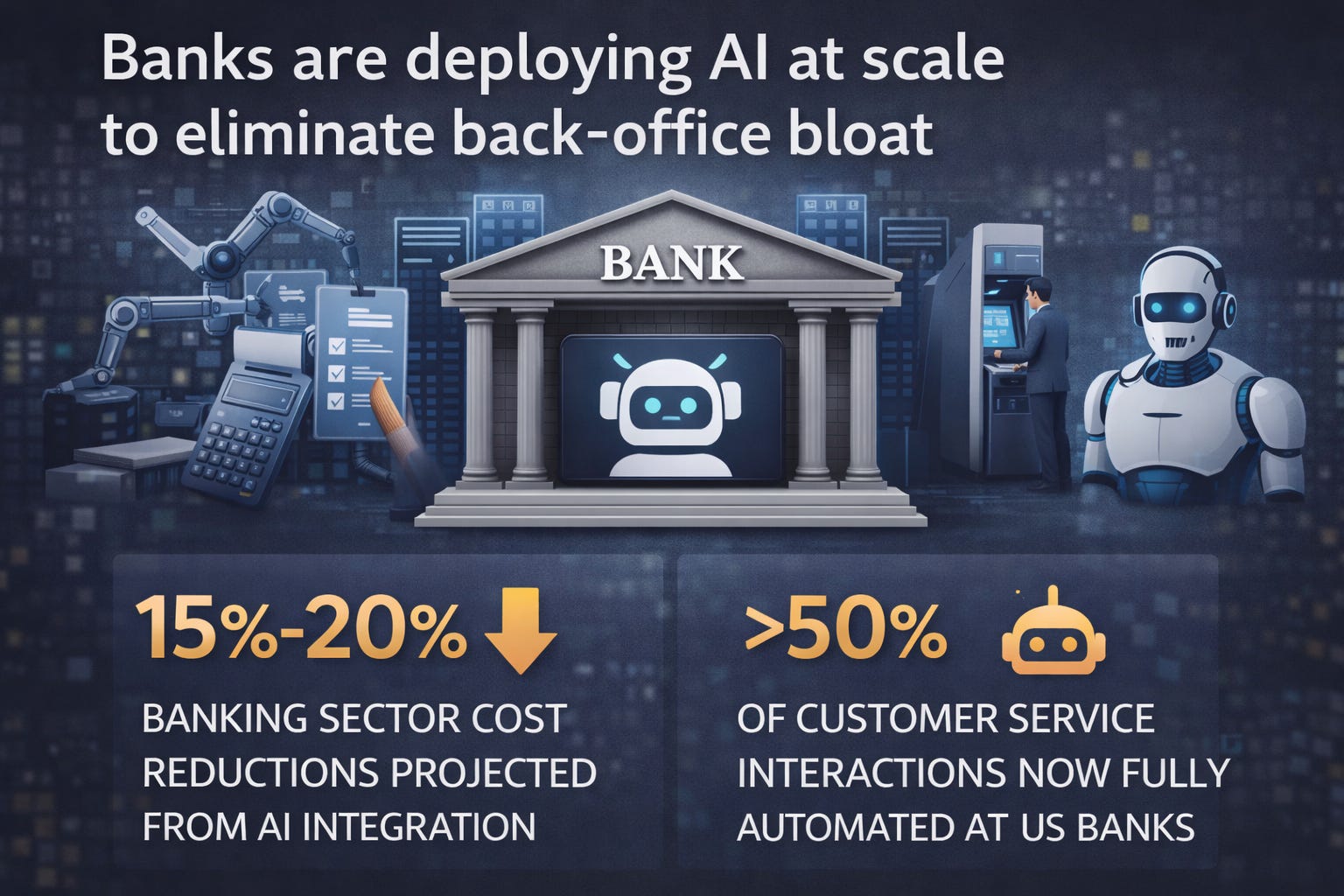

Wall Street currently treats banks like slow, boring legacy businesses. That is a fundamental miscalculation. The world’s largest financial institutions are rapidly transforming into highly efficient digital utilities, and artificial intelligence is the primary catalyst.

Banks are not just experimenting with AI; they are deploying it at scale to eliminate back-office bloat. I’ve worked for more banks than I’d like to admit and I know firsthand how inefficient their processes are. Something that should take a day, typically takes a week. There are teams of people doing meaningless tasks.

According to recent industry projections, AI integration is expected to drive 15% to 20% net cost reductions across the banking sector. In customer service alone, over half of all interactions at US banks are now fully automated.

By automating important business processes, including:

compliance checks

risk modeling

loan processing

customer support

Banks are drastically lowering their operating ratios. Every single dollar saved on administrative overhead is a dollar that falls directly to the bottom line. In a sector that already generates massive amounts of cash, this sudden drop in operating expenses translates directly into the free cash flow required to fund massive dividend increases and share buybacks over the next decade.

The Stablecoin Settlement Shift

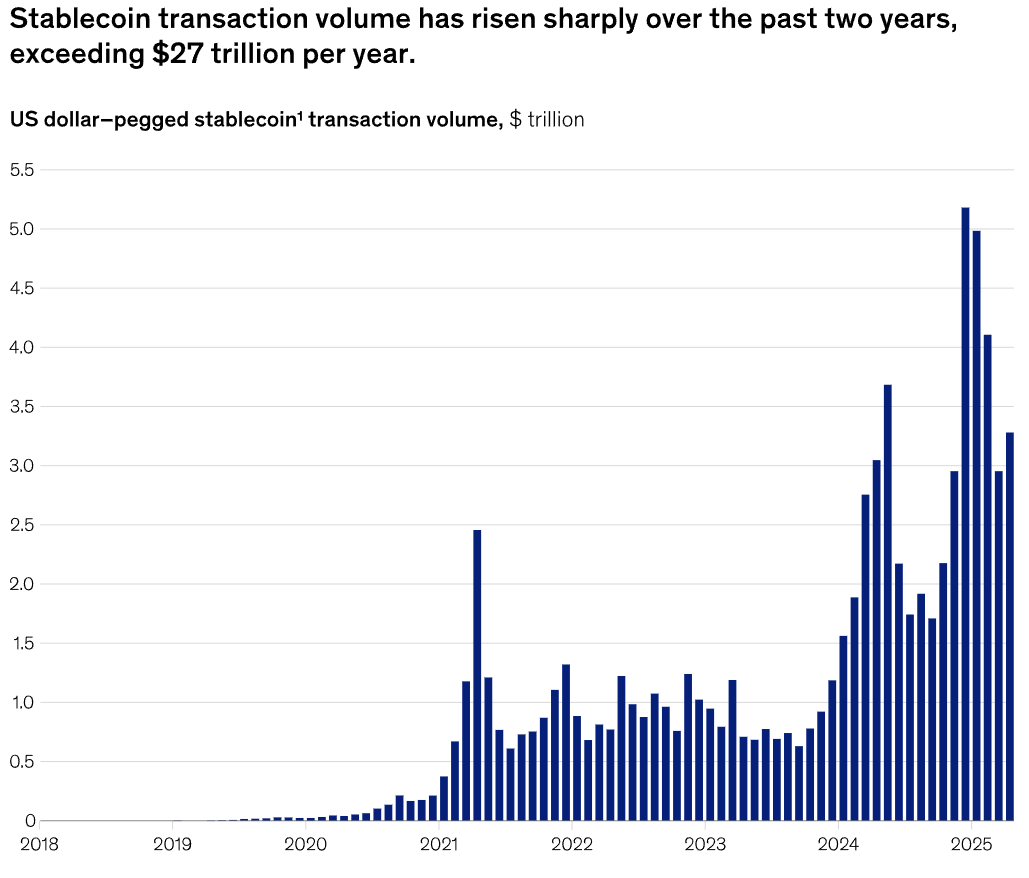

The second catalyst driving this margin expansion is the modernization of institutional plumbing. Cryptocurrency has evolved far beyond retail speculation and has become a serious utility for the banking sector.

What is a stablecoin?

A stablecoin is a type of cryptocurrency designed to maintain a stable value by pegging it to a reserve asset, most commonly the U.S. dollar, to minimize the volatility typical of digital assets like Bitcoin. They act as "digital cash" on blockchains for fast payments and trading, typically backed by fiat currency or, rarely, algorithms.

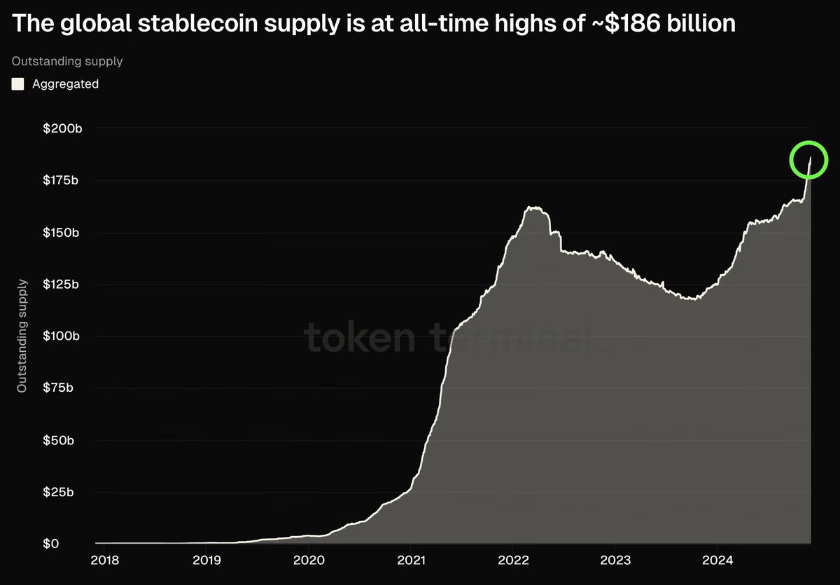

The total supply of stablecoins has exploded to over $200 billion for one incredibly practical reason:

Traditional cross-border payments and institutional settlements take days and cost a fortune.

Financial institutions are now actively adopting stablecoin and blockchain infrastructure to settle business-to-business transactions instantly and at a fraction of the traditional cost.

This specific “crypto back-office adoption” removes friction, slashes transaction fees, and frees up billions in liquidity that used to be trapped in transit. When a bank can settle a billion-dollar cross-border transaction in seconds for pennies, instead of days for thousands of dollars, their profit margins per transaction skyrocket.

From Payment Titans to Broad Income

To see this technological shift in action, look no further than the ultimate financial toll booths:

The market loves to speculate on new fintech disruptors, but these legacy titans are the ones actually capturing the tech boom. Visa, for example, is already utilizing USDC and the Solana blockchain to settle fiat-based payments with issuers, drastically reducing cross-border friction. Both networks are also deploying massive AI models to automate fraud detection and streamline merchant onboarding, further widening their economic moats.

This is exactly why I’ve continued to build a position in Mastercard. I believe the stock is very undervalued and I anticipate annualized returns of 12%-16% over the next five years. I released a dedicated analysis on Mastercard that you can read below.

However, for a dividend investor, there is a glaring issue. Visa yields roughly 0.7%, and Mastercard yields roughly 0.5%. While they are fantastic growth engines, they offer terrible current cash flow.

You do not need to settle for a sub-1% yield to profit from the financial sector’s technological upgrade, nor do you need to guess which specific regional bank will build the most efficient AI model. The most efficient, risk-adjusted strategy is to own the broader financial sector and let the collective margin expansion do the heavy lifting. To capture this sector-wide growth while generating serious cash flow, we must take a diversified approach.

This brings the strategy directly to the John Hancock Financial Opportunities Fund BTO 0.00%↑

Yield Math and Institutional Confidence

BTO is a closed-end fund that invests in a diversified portfolio of financial services companies, holding a broad basket of regional banks, capital markets businesses, and financial institutions. By taking this diversified approach, BTO naturally captures the sector-wide cost reductions.

BTO offers investors a starting dividend yield of 7.7%.

As the underlying companies in the fund reduce their overhead via AI and blockchain integration, their collective free cash flow increases. This fundamentally supports BTO’s net asset value and provides the underlying capital needed to maintain its distributions.

To understand the true income capabilities of this diversified approach, we have to look at the raw distribution math. BTO is structured to pass the success of the financial sector directly to the shareholder.