10 Monthly Dividend Stocks That Pay Me $1,688💸

The 10 monthly dividend stocks I personally own and exactly how much income each one pays me.

Most investors wait every quarter to collect their dividends.

I prefer to get paid every single month.

Over the past few years, I’ve built a portfolio designed for one thing: reliable monthly income. Today, I’m breaking down 10 dividend-paying stocks I personally own, how much they pay me each month, and why each one still earns a spot in my portfolio.

Whether you’re just getting started or looking to fine-tune your income stack, this list will give you a real-world look at how monthly dividends can create real cash flow and how I built these specific holdings up to pay me $1,688/month.

Just as a reminder, I generate an average of more than $3,000 per month in dividend income. I share those monthly dividend reports for paid subs. You can check out the latest report for April below.

April 2025 Dividend Report

The market started to see a rebound over the course of April as Trump dialed back the aggressiveness on some of the tariff policies that were going to be implemented. Whatever ends up happening, I continue to collect my dividends month after month, which I can then allocate towards discounted stocks. This month, I initiated a position in ASML Holdings (AMSL) and I plan to accumulate $10,000 of that position over the next quarter. I

My Current Monthly Income Stocks

1. Realty Income (O) — $60/month

Realty Income is often called “The Monthly Dividend Company” — and for good reason. It’s one of the most dependable income-paying stocks in the market, with over 640 consecutive monthly dividend payments and more than 100 increases since going public in 1994.

As a net lease REIT, Realty Income owns over 13,000 properties across the U.S. and Europe, leased to major tenants like Walgreens, 7-Eleven, FedEx, Dollar General, and CVS. These tenants sign long-term leases and are responsible for property taxes, insurance, and maintenance — which means consistent, low-maintenance income for Realty Income.

Monthly cash flow I can rely on — this is one of the most predictable payouts in the market

Dividend growth — while not rapid, the increases are consistent and reflect responsible management

Tenant diversification — no single tenant makes up more than 5 percent of rental revenue

Defensive — recession-resistant businesses like convenience stores and pharmacies make up a large portion of the portfolio

Realty Income is the foundation of my monthly income stream. It’s not flashy, and it won’t deliver explosive returns, but it does what I need: it shows up every month, pays me, and provides a layer of stability across the rest of my higher-yielding, more volatile income positions.

⚠️ Risk Considerations:

Rising interest rates can pressure REIT valuations, as their yields must compete with safer bonds

Retail-focused real estate can be sensitive to changes in consumer behavior and economic slowdowns

Realty Income tends to issue new shares to fund growth, which can dilute shareholders if not managed properly

Despite these risks, the track record speaks for itself. The dividend has never been cut, even during the Great Financial Crisis or COVID-19, and the company continues to expand through acquisitions and international growth.

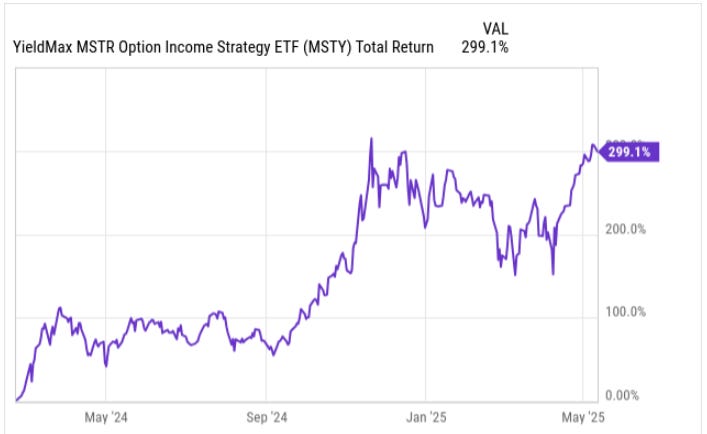

2. MSTY – YieldMax MSTR Option Income ETF — $600/month (average)

This is easily the most aggressive position in my entire income portfolio — and one of the most rewarding. MSTY isn’t a typical dividend stock. It’s a synthetic option ETF designed to squeeze massive monthly income out of MSTR’s volatility, and right now, it’s doing exactly that.

The fund currently yields over 80 percent annualized based on recent distributions. That number fluctuates month to month, but even the low end of MSTY’s payout makes it one of the highest income-generating assets available to retail investors today.

MSTY doesn’t actually own shares of MicroStrategy (MSTR). Instead, it mimics its price movement using a combination of long calls and short puts while layering in a covered call strategy to generate premium. That premium gets passed on to shareholders as monthly income.

Because MSTR is so closely tied to Bitcoin — and because Bitcoin is wildly volatile — the options on MSTR carry huge implied volatility. This allows MSTY to sell calls at high premiums and deliver monthly cash flow that far exceeds traditional equity yields.

In my case, it’s generating around $600 per month — and that number was even higher during peak BTC momentum.

Here’s where it gets tricky.

MSTY’s price has fallen more than 48 percent since launch

But its total return, including dividends, is positive 48 percent over the last year

This tells you everything. The fund’s value erodes over time, but the income offsets the drawdown — and for now, it’s still producing far more than most traditional investments.

Just be aware: MSTY will never fully capture the upside of MSTR. That’s the tradeoff. You’re giving up growth for extreme income. If MSTR surges 100 percent, MSTY might only capture a fraction of that. But in return, you’re getting paid every month — and fast.

I specifically covered MSTY in my Series.

⚠️ Risk Factors You Need to Know:

This is not a sleep-well-at-night fund. Here’s what to consider before holding:

Crypto correlation — MSTR is essentially a Bitcoin proxy. If BTC tanks, MSTY will suffer

Distribution volatility — payouts have been declining in recent months

NAV erosion — over time, capital will degrade unless markets keep moving up

Tax implications — some distributions are return of capital, others are ordinary income

I don’t own MSTY for growth. I own it for cash flow.

Every month it drops hundreds of dollars into my account, which I can then reinvest, use to offset expenses, or build toward financial independence.

I consider MSTY a high-risk, high-yield tool — not a foundational holding. It’s a calculated bet on volatility. And while the crypto cycle may shift in the coming months, for now, MSTY continues to earn its place in my income stack.

3. MAIN – Main Street Capital — $18/month

MAIN is one of the few business development companies (BDCs) I trust enough to hold long term. It specializes in lending to and investing in small to mid-sized private companies — a niche market where traditional banks often hesitate. Look at how ridiculously diversified MAIN is.

What sets MAIN apart from other BDCs is its conservative management, strong balance sheet, and impressive dividend track record. It pays a reliable monthly dividend, with bonus special dividends sprinkled in throughout the year when performance warrants it.

Consistent monthly income backed by real operating businesses

Strong dividend discipline and history of special payouts

Offers equity-like upside with bond-like cash flow

A more stable, internally managed BDC, which aligns incentives with shareholders

MAIN is not a flashy growth stock, but it brings steady yield with quality underwriting — exactly what I want from this type of holding. It’s one of my lowest-maintenance positions, and the passive income just keeps rolling in.

🧰 Tools to Build Your Own Income Stack

Want to get a well-rounded idea of where to start your investing journey? I have you covered here as well!

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

4. FEPI – REX FANG+ Innovation Premium ETF — $100/month

FEPI is one of my more balanced income plays in the synthetic space. It tracks the FANG+ Index — which includes big names like Apple, Amazon, Meta, Microsoft, Nvidia, and Tesla — but layers on an options income strategy to produce monthly cash flow.

What makes FEPI different is that it spreads its exposure across multiple high-growth tech names rather than focusing on a single stock. That gives it a more diversified risk profile compared to single-name YieldMax ETFs like AMZY or FBY.

The fund sells call options on the index to generate premium and distribute it monthly. While the yield isn’t as extreme as something like MSTY or CONY, it’s still strong — and feels more sustainable due to the diversified basket.

Broad tech exposure without needing to hold each stock individually

More stability than single-stock synthetic funds

A cleaner way to monetize tech sector volatility without going all in on one company

It fits well between my lower-risk holdings (like O) and high-octane positions (like CONY)

I see FEPI as a solid middle-ground holding. It gives me a piece of the innovation story and pays me monthly — without making me overly reliant on the fate of just one stock or crypto momentum.

5. PDI – PIMCO Dynamic Income Fund — $30/month

PDI is one of the few non-tech, non-options-based income positions I hold — and for good reason. It’s a bond-heavy closed-end fund managed by PIMCO, one of the most respected fixed-income managers in the world.

The fund invests in a mix of corporate credit, mortgage-backed securities, and emerging market debt, often using leverage to amplify returns. While it doesn’t offer the same eye-popping yield as some synthetic funds, the income is steady, and the fund has a long track record of paying monthly.

Diversifies my portfolio away from equity and tech

Offers a more traditional, interest-driven income stream

Managed by a team that knows how to navigate rate cycles

Balances out the risk from my high-volatility positions like CONY or AMZY

It’s not flashy, and the NAV has taken hits in rising rate environments — but I hold PDI as a counterweight to the more speculative income sources in my stack.

5 Monthly Paying Dividend Stocks Yielding More Than 40%

In a world where most dividend stocks yield between 2 and 4 percent, finding consistent double-digit income feels like hitting the jackpot. But today, we are not just talking about high yield. These stocks are yielding more than 40 percent annually, and they pay you

6. AMZY – YieldMax AMZN Option Income ETF — $200/month (avg)

AMZY is my synthetic income layer on Amazon — a stock I’ve always respected, but never bought for dividends (because it doesn’t pay one). This fund solves that by using a covered call strategy to generate monthly income from Amazon’s stock price movement.

Like other YieldMax ETFs, AMZY doesn't actually own Amazon shares. Instead, it uses options to replicate exposure and then sells calls to generate high-yield premium. The income is substantial — at times north of 50 percent annualized — and while the fund gives up some upside, it rewards me with consistent monthly cash flow.

I get exposure to Amazon’s stock without waiting for it to pay a dividend

High monthly payouts that help cover real expenses

Volatility in AMZN fuels strong options premium

Ideal for my income strategy — especially during choppy or sideways markets

AMZY won’t beat Amazon over the long term in total return, but it wasn’t built for that. It’s a cash flow play, and right now, it’s paying me extremely well to hold it.

7. CONY – YieldMax Coinbase Option Income ETF — $300/month (avg)

This one’s volatile — no surprise there. But the option premiums are massive. It pays well even if the stock doesn’t move much.

Why I own it: Extremely high yield potential tied to a high-beta stock. Not for everyone, but it works for my income strategy.🧠 How CONY Generates Yield

CONY doesn’t hold Coinbase shares outright. Instead, it uses a synthetic option strategy that mimics COIN’s price movements. It simultaneously uses long calls and short puts to simulate exposure, while writing covered call options on top to generate premium income.

Because COIN is a high-beta stock tied to crypto sentiment, its implied volatility is massive. That’s exactly what makes CONY work. The more volatile the underlying asset, the more premium the fund can earn — and the more cash it distributes to shareholders.

Premiums are typically harvested weekly, but payouts are distributed monthly. This allows CONY to consistently deliver some of the highest income among all YieldMax funds.

Like other funds in this category, CONY’s share price doesn’t tell the full story.

Price performance since inception: deeply negative

Total return (including dividends): still competitive, though less impressive than MSTY

CONY, in many ways, is a bet on staying paid, not staying green. The idea isn’t to grow your capital — it’s to get your investment back in cash distributions as quickly as possible, then ride on house money.

For example, if you invested $10,000 and CONY continues yielding at or above 60 percent annually, you could receive back most or all of your principal in 18 months, through income alone.

COIN is highly reactive to crypto markets. When Bitcoin spikes, Coinbase usage increases, and the stock tends to follow. That volatility jacks up options premiums — which fuels the yield. During bullish crypto waves, this creates rich, consistent payouts for CONY holders.

But the reverse is also true. If the crypto market stalls or crashes, COIN can fall rapidly — and CONY’s NAV can erode just as fast. Worse, in low-volatility environments, the fund earns less premium, leading to declining dividends.

That’s what we’ve started to see recently. As crypto cooled off in Q1 2025, CONY’s payouts began shrinking. While the fund still produces high yield relative to traditional investments, it's a reminder that income is not fixed — it moves with the market.

⚠️ What to Watch Out For

Like MSTY, CONY is a tactical income tool, not a buy-and-forget asset. Here are the biggest risks:

NAV decline over time, especially if Bitcoin enters a bear cycle

Distribution cuts if option premiums shrink

Volatility drag from COIN’s unpredictable price action

Tax complexity, especially with short-term gains and potential return of capital

No underlying stock ownership — meaning no traditional dividend support

If you hold this in a taxable account, keep in mind that a portion of the payouts may be taxed as ordinary income, while others may be classified as return of capital — which reduces cost basis but delays the tax hit until sale.

I don’t expect CONY to last forever. But while it’s paying, I want to be collecting.

Right now, it’s producing some of the highest monthly income in my entire portfolio. That cash flow gives me flexibility — to reinvest into safer names, cover living expenses, or simply buffer my cash position.

I treat CONY like a short-duration income trade. It’s not a forever hold. It’s a strategic allocation to monetize crypto volatility in a way that doesn’t require trading options manually or owning crypto outright.

As long as the fund keeps paying and I stay aware of the risks, it plays a valuable role in my income stack.

8. THW – abrdn World Healthcare — $50/month

THW is my healthcare anchor. It’s a closed-end fund that delivers monthly income from a globally diversified portfolio of healthcare and biotech stocks. While most of my high-yield plays lean into tech or synthetic options, THW offers something different: defensive sector exposure tied to a macro trend that’s not slowing down — increased global healthcare spending.

As populations age and medical advancements accelerate, both government and private spending on healthcare continue to rise. According to the World Health Organization, global healthcare expenditures are expected to grow significantly over the next decade — and THW is positioned to benefit.

The fund holds a mix of major pharma companies, biotech innovators, and healthcare services firms. It also uses a covered call overlay to generate additional income, which is what fuels its above-average yield.

Healthcare is recession-resistant and growing globally

THW pays a reliable monthly dividend, currently yielding around 9 to 10 percent

Diversifies my income portfolio away from tech and credit

Offers exposure to long-term healthcare trends while still delivering high yield

THW helps me balance out my portfolio by anchoring it in a non-cyclical sector — and still paying me monthly while I wait. In a world where medical spending keeps rising, I’m happy to keep collecting.

9. GOF – Guggenheim Strategic Opportunities Fund — $70/month

GOF is a high-yield closed-end fund focused on credit and structured income.

Why I own it: High yield, long track record, and pairs well with my equity-focused funds. I previously wrote an in-depth analysis about this fund.

This Fund Has Paid A Double-Digit Dividend For Nearly 2 Decades

Most people have no idea that you can collect a double digit dividend yield over a long period of time. I’d argue that a lot of people don’t even know what a dividend is. If you’re reading this, I’m sure you’re not one of these people. They let ignorance take over and they accept a measly 0.1% interest rate on thei…

10. YMAX – YieldMax Universe ETF — $180/month

This ETF combines several YieldMax single-stock strategies under one ticker.

Why I own it: Built-in diversification across multiple synthetic income streams with excellent yield. This one actually pays WEEKLY.

Series: Building A Second Income Stream (Part 1)

This has to be the best time in modern history to be an income investor. There are so many different tools at our disposal that make it incredible simple to increase our income, wealth, and financial security. I wanted to share the foundation of a new

🧠 Final Thoughts

This portfolio is not built for speculation. It’s built for cash flow.

Some of these stocks are riskier than others. Some will underperform in a bull market. But that’s the tradeoff I accept for the reward of consistent, scalable, and reliable monthly income.

My advice? Don’t copy this list blindly. Use it as a template. Adjust for your own risk tolerance and income goals. And most importantly — start building your own stack of income.

The sooner you start, the sooner you stop depending on paychecks.

I hold a few of these dividend stocks. This is a good list to get started with. Thanks for sharing.