Actionable Steps To Instantly Improve Your Financial Situation

These are bite-sized actions that you can knockout in a few mins.

Getting your financial foundation in order can be a scary process. Almost all of my focus on this Substack is related to investing continue and growing your passive income. However, you must learn to walk before you can run. If your financial foundation isn’t strong, you may never find yourself in a place that feels prepared to start investing. So I wanted to share some very quick tips and actionable items that you can take to significantly improve your financial health. These are easy steps to take that don’t require you to be ‘good with money’.

Tip #1: Start Tracking Your Net Worth

Your net worth is determined by adding all of your owned assets up. This includes the value of your home, 401K balance, savings account, car value, and every other valuable thing that you own. You then subtract this total by the total amount of money you owe. This includes things like your mortgage, car loans, student loans, credit card debt, and any other miscellaneous debt you may have,

Nowadays, this process is simplified and can automatically be calculated for you. I personally use Empower’s Net Worth Dashboard. The tool is completely free! You simply login to your accounts and the aggregator consolidates everything into a neat looking template for you. You can easily see your assets and liabilities to get a clear understanding of your entire financial picture.

You’ll be able to measure how much cash you bring in every single month and compare it against the amount of money you are spending. You will be able to effectively gauge where most of your money is being spent. Empower assists you by breaking down how much you are spending on food, transportation, and other categories. You can set spending targets as well.

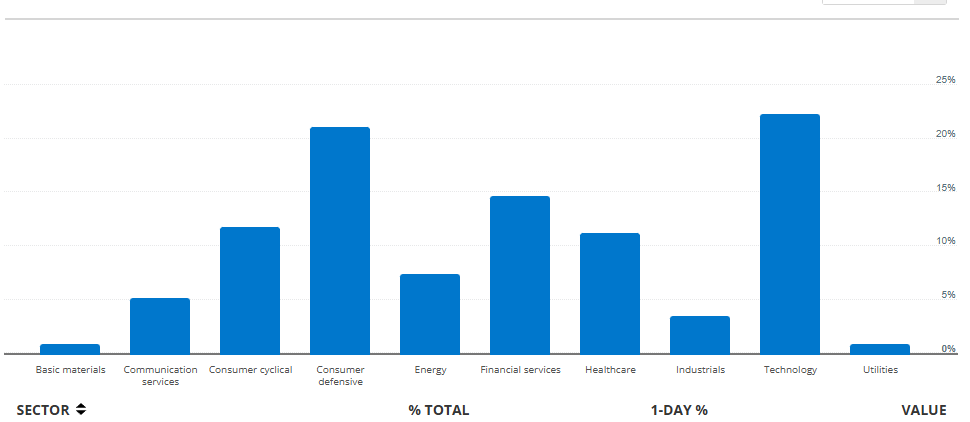

The tool also provides free insights into any investment portfolios you have. You can see an exact breakdown of your assets and their respectively sector allocation. For example, here is a snapshot of only one of my portfolios and how my assets are allocated.

The site / app automatically updates every single time you login and creates an easy-to-understand chart of your assets and net worth over time. I would highly recommend this dashboard and it’s an easy way to improve your knowledge of your entire financial picture.

Tip # 2: Switch To A High Yield Savings

If you aren’t already at a banking institution that offers a high yield savings account, you need to switch as soon as possible. Most institutions are FDIC insured nowadays but it takes a simple google search to find the right fit for you. I like to use Nerd Wallet as a trusted source but feel free to use your own research.

Plenty of the popular banks like TD Bank, Santander, Wells Fargo, and Bank of America give its customers an interest rate that is below 1% on savings accounts. There is absolutely no reason for you to be collecting such a little amount of money on your savings that you keep in the bank. Looking at the picture above, there are some banks offering an interest rate of over 4% at the moment.

Tip # 3: Pay Off Your Smallest Debt

It’s extremely difficult to get ahead if a large percentage of your income is going towards loan payments. Whether it be credit cards, car loans, student loans, or anything else. If you have the means to, pay off the smallest debt that you have. Traditional advice will tell you to pay off the debt balance with the highest interest rate first. This makes the most mathematical sense but we aren’t here for that. What I want you to do is obtain those small wins that get you a step further in your financial journey.

If you have a little $500 balance on your credit card, but you have $2500 in the bank… go ahead and pay that balance off. By continuing to make the minimum payment for the next twelve months, you are actively choosing to pay more than you owe (because of interest). By knocking it out of the way in advance, you are now freeing up a monthly expense that you have and those funds can be repurposed into another area of your life.

Eliminating that $25 monthly minimum from your expenses every month means you now have an extra $25. You can now afford to put an extra $25 towards the next smallest debt balance you are holding. You can keep snowballing this process up until your eventually knock out all of your smaller debt balances. Keeping these debt balances around unnecessarily is a way to ensure that you never get ahead.

This tip may require a little more planning on your end but that’s okay! You got this!

The Money Playbook To Get Your Finances Straight

Some people put this taboo around money that makes it such an uncomfortable topic of conversation for most. I always found it strange that talking about money wasn’t embraced by the same people that would openly discuss drugs, sex, and gossip. As I’ve grown older I’ve come to learn that people’s hesitation to talk about money usually comes from the lack…

Paying off the highest interest credit card has not been working, but paying the smallest credit card balance off has. The high interest card eats up my payments, which makes it hard to stay ahead of the interest fees. This article is super helpful.