Everything Is Getting More Expensive. Here’s What To Do

Inflation is not going away. But you can fight back by owning assets that pay you every month

Groceries are more expensive. Rent is going up. Gas, insurance, streaming services, and basic everyday items all cost more than they did last year. Even if inflation slows down on paper, most people still feel it in their wallets. And once prices rise, they rarely go back to where they were.

It is not just one category.

The cost of food has jumped.

Housing is harder to afford whether you rent or buy.

Healthcare premiums are rising.

Used cars are still overpriced.

Even the “cheap” fast food combo you used to get for under ten dollars is now closer to fifteen.

Everything costs more, and there is no sign of a return to normal.

You are not imagining it. Life is more expensive than it used to be.

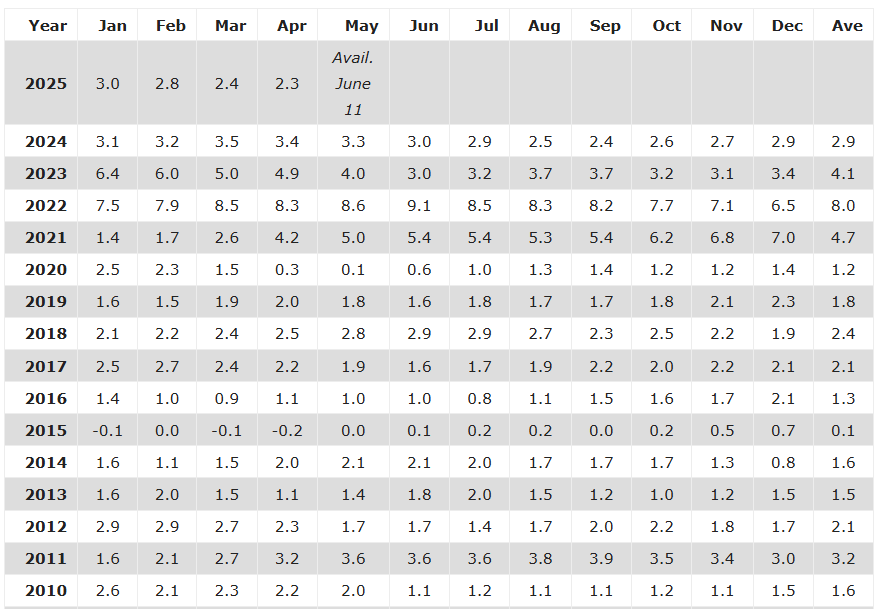

Over the last four years, inflation has climbed faster than any time in recent history. In 2021, the average inflation rate was 4.7 percent. In 2022, it spiked to 8 percent. Even in 2023, long after headlines said it was “cooling,” prices were still rising at over 4 percent. And while 2024 and 2025 look tamer by comparison, they are still well above the decade average that hovered between 1.5 and 2 percent.

What this means is simple. Prices have permanently reset higher. Even if the rate of inflation slows, the damage is done. You are now paying more for the same things — and your cash is worth less every year it sits idle. Look at the inflationary table below:

So what can you actually do about it?

Cutting back on coffee won't move the needle. What will move the needle is changing your position in the economy. You do that by owning assets.

Own What Benefits From Inflation

When you invest, you become an owner of productive assets. That includes businesses, real estate, and funds that generate cash flow. These assets do something your savings account cannot. They respond to inflation.

A grocery store raises prices. You feel it at checkout. But if you own shares in that company, the increased revenue flows back to you through higher profits or dividends.

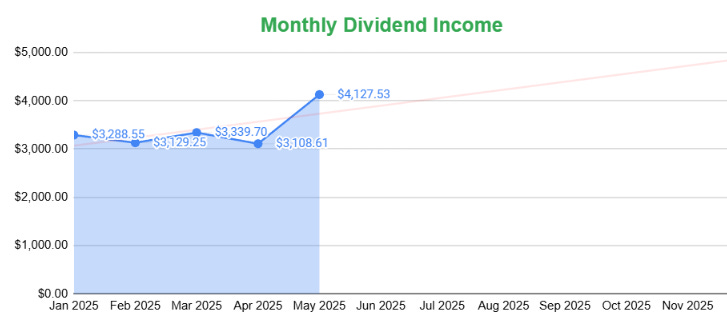

A real estate trust raises rent. You feel it if you are a tenant. But if you are a shareholder in that REIT, the income helps cover your cost of living. By following this strategy, I was able to eventually accumulate several thousands in dividends every single month.

The point is that you either feel the squeeze or you collect the reward. Investing allows you to stop being on the losing side. As a starting point, here are 6 stocks that I’d feel comfortable holding forever.

6 Stocks I’d Be Comfortable Holding for the Next 20 Years

Most people spend more time trying to beat the market than actually building wealth. They stress over charts, chase the next big trend, jump in and out of trades, and end up holding a scattered mess of stocks with no clear purpose.

Dividends That Offsets Higher Costs

The smartest thing you can do right now is build a stream of recurring income. Not income from your job, but income that shows up whether you work or not.

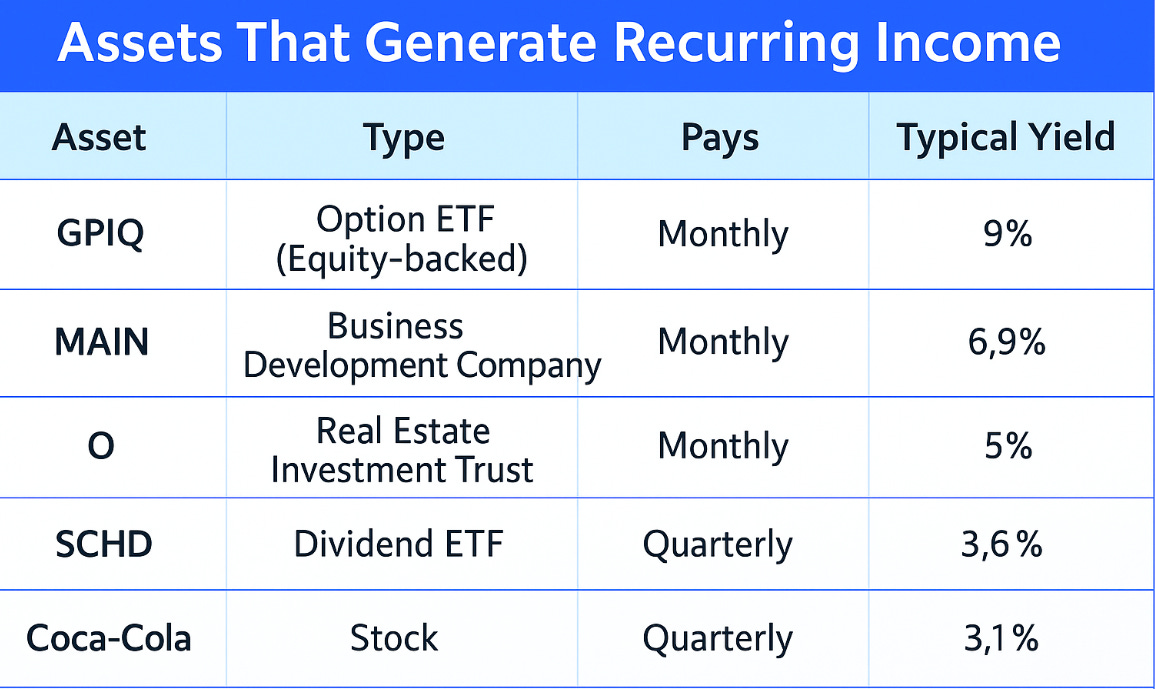

Here are a few examples of assets that produce consistent income:

You do not need to guess when these pay you. Most of them distribute income like clockwork. That money can be used to pay bills, reinvest, or slowly reduce your reliance on job income. For a second, let’s specifically focus on Coca-Cola. The company has the kind of global reach, customer loyalty, and pricing power that lets it adjust as inflation rises. When input costs go up, Coke raises its prices. Consumers pay more, and revenue stays strong.

And when revenue stays strong, so do dividends.

Coca-Cola has paid a dividend every year since 1920. It has raised that dividend for over sixty consecutive years. That puts it in elite company as a Dividend King, a business that raises its payouts regardless of the economy.

When inflation eats into your cash, Coca-Cola increases your income.

If you own shares of KO, you are not just investing in a company. You are buying into a system that:

Raises prices with inflation

Maintains customer demand

Sends cash back to you every quarter

Historically appreciates in value over time

So while everyday people are paying more at restaurants, at grocery stores, and at vending machines, Coca-Cola shareholders are collecting more income. That is the position you want to be in. Not just spending into inflation, but profiting from it.

Why This Might Be the Greatest Dividend Growth ETF Ever Created

We are living in an era where inflation is no longer a background risk. It is front and center. While it has cooled from its 2022 peak, core inflation in the United States still hovers above the Federal Reserve’s two percent target, and many essential goods and services continue to rise in price year over year.

Buy and Hold: Why Temporary Losses Do Not Matter

A lot of people get scared when they see their investments go down in value. They hear terms like "market volatility" or read headlines about corrections and crashes, and suddenly, stocks feel like a gamble.

But here is what most people do not realize: everything else you buy loses value too.

Buy a car and it drops twenty percent the moment you drive it off the lot. Buy clothes and they wear out over time. Buy furniture and it depreciates. Even the phone or laptop you are using right now is worth less today than it was six months ago. We accept this kind of loss as normal.

But when a stock dips temporarily, people panic.

The truth is that buying shares of high-quality companies is not like buying a car. You are not spending money. You are converting it into ownership. Ownership that can grow. Ownership that can pay you income. Ownership that can last for decades.

That is the essence of a buy and hold strategy.

When you buy and hold dividend-paying companies, your focus shifts from price to income. You stop asking what the stock is worth today and start asking how much income it is generating for you this year.

Over time, this approach compounds.

The share price of Coca-Cola might go up and down from week to week, but if you hold it for five, ten, or twenty years, the income you collect continues to grow. And so does your ownership stake if you reinvest. The market rewards patience. It always has.

Historically, long-term investors who hold diversified portfolios through good times and bad tend to come out ahead. They do not try to time the market. They do not jump in and out. They buy assets that generate cash and let them work.

You Do Not Need to Start With Much

Too many people assume you need tens of thousands of dollars to build an income machine. That is false. You can start with one hundred dollars. You can buy a share of an income-producing ETF, collect your first payout next month, and reinvest. Over time, those small snowballs become powerful cash flows.

You are not going to beat inflation with budgeting alone. You beat inflation by building a portfolio that works while you sleep.

The sooner you start, the sooner the pressure lifts. I’d recommend reading the article below if you are still in the beginning phases of the journey.

What I’d Do With $1,000 Right Now If I Wanted to Start Building Passive Income

Let’s be real. One thousand dollars is not life-changing money.

Inflation will always exist. Sometimes it will be two percent. Other times it might be eight. You cannot control that. What you can control is how exposed you are to it.

When all your income comes from a job, you are vulnerable. When part of your income comes from assets, whether it is dividends, rent, or royalties, you shift the balance of power.

You stop relying on prices staying low and start relying on your portfolio delivering income.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters