How I Use Margin Safely to Increase My Dividend Income

These are the rules you MUST follow to safely use margin to amplify your dividend income.

Margin is money you borrow from your brokerage firm to invest. You are borrowing money and using your stocks as collateral.

It lets you buy more assets than you could with just your own cash, but you have to pay interest on the borrowed amount.

Most people treat margin like a financial boogeyman. The horror stories are everywhere: accounts getting wiped out, margin calls in bear markets, reckless bets that blow up entire portfolios. And to be fair, those stories are real.

But margin itself is not the problem. The problem is how people use it. Same as with credit cards.

When applied with intention and discipline, margin can become one of the most powerful tools in an income investor's toolbox. It allows you to accelerate cash flow, reinvest faster, and unlock opportunities that might otherwise take years to reach. I am going to walk you through exactly how I use margin in my portfolio. You will see the math. You will see the rules I follow. And you will see why I believe most investors are too scared of something that could actually bring them closer to financial independence if used correctly.

This is not for everyone. But if you have a high yield portfolio and want to put your assets to work more efficiently, this strategy might open some doors.

What Margin Is and Why I Use It

Margin is borrowed money that allows you to buy more assets than your cash alone would allow. In a brokerage account, it usually means borrowing against the value of your existing investments to buy additional shares. That borrowed money comes with interest, and it can amplify both your gains and your losses.

Most people hear that and instantly think it sounds dangerous. And it can be, if you treat margin like free money or use it to chase risky trades.

But here is where things shift.

I am not using margin to swing for the fences. I am using it to increase exposure to high yield dividend funds that pay me every week or every month. These are assets designed to throw off cash. When used strategically, they create a consistent income stream that can outweigh the cost of borrowing.

Think of it like this:

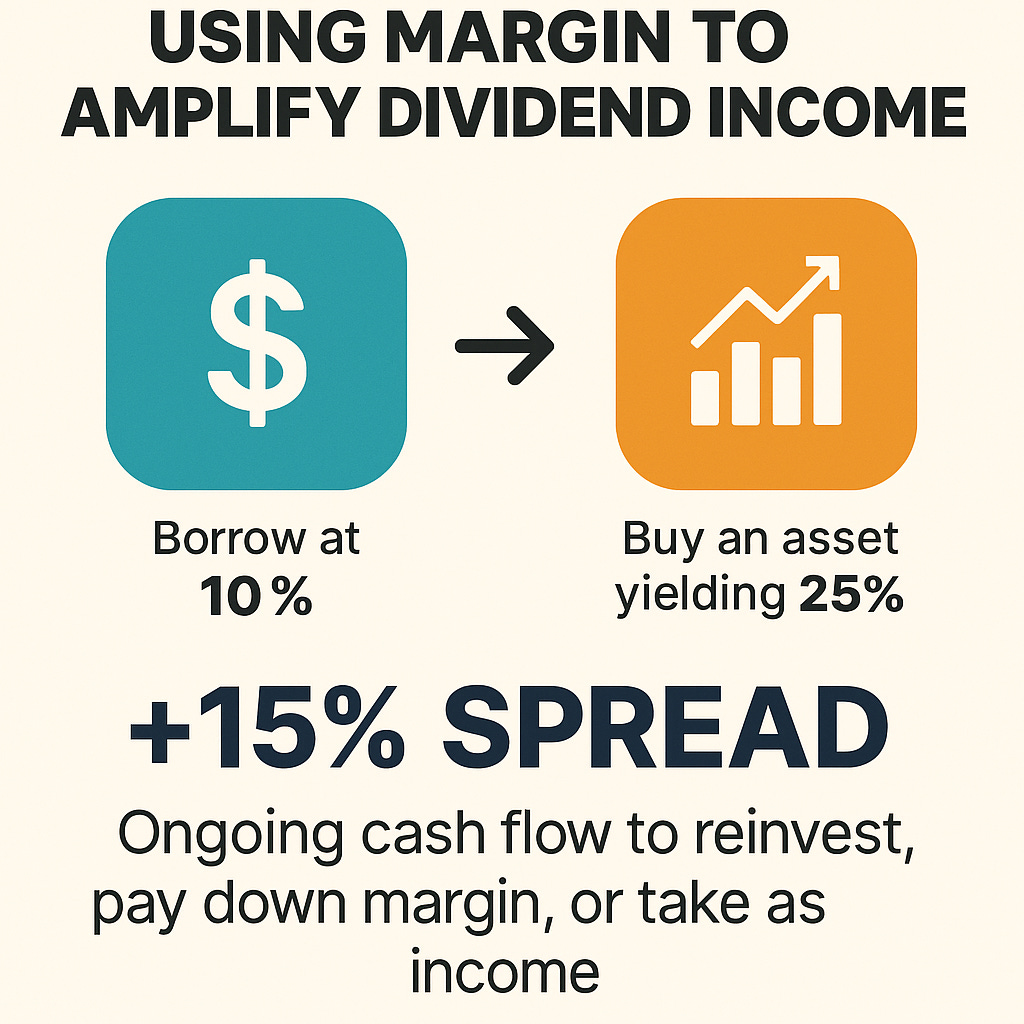

If I borrow at 10% and buy an asset yielding 25%, I am generating a 15% spread. That spread becomes weekly or monthly cash flow that I can reinvest, use to pay down the margin, or take as income. This is how I am able to generate weekly income that packs bill-paying power.

This is not about timing the market or finding the next hot stock. It is about turning idle portfolio value into an income engine. Margin allows me to access income I would not otherwise have without selling my long term holdings or waiting years to save more cash.

Used with the right rules in place, it becomes a cash flow strategy with measurable math and manageable risk. In the next section, I will walk you through the exact rules I follow so I never lose sleep over my margin balance.

This process of using margin to amplify my income is how I was able to generate nearly $4K in dividend income in June. For those unfamiliar, I publish dividend income reports every single month for readers.

My Rules for Using Margin Safely

Margin is powerful, but it is also unforgiving if misused. That is why I follow a strict set of personal rules to keep it working for me and not against me. These rules are designed to limit downside, preserve flexibility, and ensure that I never put myself in a position where a market dip forces me to sell.

Here is what I follow:

1. Limit Margin to 20% or Less of Total Portfolio Value

I never want my margin loan to exceed 20% of my total portfolio. This gives me breathing room if markets drop and ensures I can cover margin calls with cash or dividends rather than selling assets at a loss.

2. Only Use Margin for Cash Flow Assets

I never use margin to buy growth stocks, speculative trades, or anything that does not produce income. My goal is to buy assets like high yield ETFs, BDCs, or covered call funds that pay me reliable dividends. That way, I am using margin to create positive cash flow from day one.

3. Interest Must Be Covered by Dividends

If I am paying 10% interest, the asset I buy must yield more — ideally much more. I aim for at least a 15 to 20% yield on the capital I borrow. This creates a positive spread and makes the strategy self-funding. However, YieldMax funds that pay over 40% make this spread so much larger.

A Weekly Paying Dividend ETF With an 80% Yield? Meet ULTY

In recent years, option income ETFs have surged in popularity as investors look for more control over their cash flow. Traditional dividend stocks often pay quarterly and yield two to four percent annually. That might be enough to supplement a portfolio, but it is rarely enough to build a financial foundation that can support real lifestyle goals…unless you are working with a million dollars or more.

4. Always Keep a Cash Buffer

I keep a chunk of cash or liquid assets available to reduce margin quickly if needed. This buffer protects me from forced selling and gives me options if the market turns.

5. Reinvest or Deleverage Strategically

If cash flow exceeds my needs, I use it to either reinvest into more dividend-paying assets or pay down the margin. This creates a flywheel effect that builds over time — but I am always checking the math to ensure the income justifies the leverage.

6. Never Use Margin on Margin

I never borrow more to cover margin interest or compound risky bets. Everything I borrow is backed by a clear income plan. The moment it feels forced or speculative, I scale back.

My Cash Flow Math

This is where the strategy comes to life and where most people either get excited or scared off. The numbers do not lie, and when used carefully, margin can generate meaningful weekly or monthly cash flow that beats most traditional dividend portfolios.

Let’s run through a simple example using real-world assumptions.

Example:

You borrow $30,000 at a margin interest rate of 10% annually

This creates an interest cost of $3,000 per year, or about $250 per month

You invest that $30,000 into a high yield fund paying 25% annually

That generates $7,500 in annual dividends, or about $625 per month

Net Monthly Cash Flow:

Income: $625

Margin Interest: -$250

Net Gain: $375 per month

Now imagine that income is paid weekly instead of monthly. That is what makes funds like ULTY so powerful. The shorter cash flow cycle gives you more flexibility to reinvest, pay down debt, or simply use the income however you want.

Over time, this margin-powered income can be reinvested into more high-yield assets, creating a compounding loop. You are not relying on capital appreciation to make this work. You are using yield to create spread and that spread is real cash you can use.

7 Weekly Paying Dividend Stocks I Am Using to Boost My Income

One of the biggest mindset shifts I’ve made as an investor is this:

Of course, this only works if the underlying assets keep paying. That is why I monitor my holdings closely, stay diversified across multiple income funds, and never assume the income is guaranteed forever.

This math is simple, but powerful. And when combined with discipline and risk management, it creates one of the few paths where margin can work in your favor without turning into a gamble.

The Dividend Flywheel Effect

Once the cash flow starts, the real magic happens through reinvestment. This is where margin stops being just a boost and starts becoming a compounding machine.

Here is how it works:

Each week or month, the income from your margin-financed assets hits your account. Instead of spending it, you can reinvest that income into more high yield positions. Those new shares generate their own dividends, which then get reinvested again. Over time, this creates a snowball of growing income.

Because the cash flow is frequent, you do not have to wait long to see results. Weekly payers like ULTY 0.00%↑, YMAX 0.00%↑, XDTE 0.00%↑, QDTE 0.00%↑, QDTY 0.00%↑, or YMAG 0.00%↑ make it possible to compound faster than traditional quarterly dividends. The momentum grows quicker and becomes more predictable.

And here is the key: you are not adding new capital. You are using margin to unlock cash flow that funds more shares, which then generate more cash flow. If you stay disciplined and reinvest strategically, this flywheel can keep spinning with minimal new investment on your part.

Eventually, this income can cover expenses, pay down the margin loan, or fund diversification into other assets. It becomes more than just yield. It becomes a system.

That is how margin turns from a tool into a strategy.

How I Use The Dividend Wheel Strategy With A $350K Portfolio

I have approximately ~$500K invested across a plethora of different accounts that all work in conjunction with one another. This only includes cash that has been allocated towards stocks and doesn’t include any Crypto or Real Estate. I’m working on an efficient way to release a full portfolio breakdown at some point in the future but for now, I wanted to provide a small glimpse into what my holdings and dividend income levels look like.

How I Manage Risk and Avoid Margin Mistakes

Using margin to grow income can work, but only if you stay in control. Without guardrails, leverage can turn against you fast. That is why I treat risk management as the most important part of this entire strategy.

Here is how I protect myself:

1. I Monitor My Loan Ratio Constantly

I never let my margin loan get too large relative to my account value. My target is 10 to 20% of total portfolio value. If markets drop and that ratio climbs, I reduce the loan or add cash immediately. No guessing. No waiting.

2. I Keep Cash on the Sidelines

I always keep some cash or liquid funds ready to act as a buffer. If a margin call ever became possible, I would rather inject cash than sell long term positions at a loss. This gives me peace of mind and flexibility.

3. I Stick to High-Yield, Income-Producing Funds

I only use margin to buy assets that are already paying strong dividends. That way, the income supports the loan. I do not borrow to chase growth or speculation. If a fund’s income drops, I reassess quickly and adjust.

4. I Run the Math Before Every Buy

Every time I use margin, I ask: what is the expected yield and what is the interest cost? If the spread is not wide enough, I do not make the trade. Simple rules like this keep me from stretching just to chase yield.

5. I Have a Clear Exit Plan

If rates spike or income drops, I am ready to deleverage. I treat margin as a tool, not a crutch. If the risk-reward balance changes, I can unwind the position without panic. That includes selling income assets or using cash to pay it down.

6. I Accept That This Is Active, Not Passive

Margin requires attention. It is not something I set and forget. I check my balances regularly. I track my interest. I look at the income flow and decide whether it still justifies the exposure.

By keeping these rules tight, I avoid the common traps that ruin people who misuse margin. I am not betting on luck. I am building with intention.

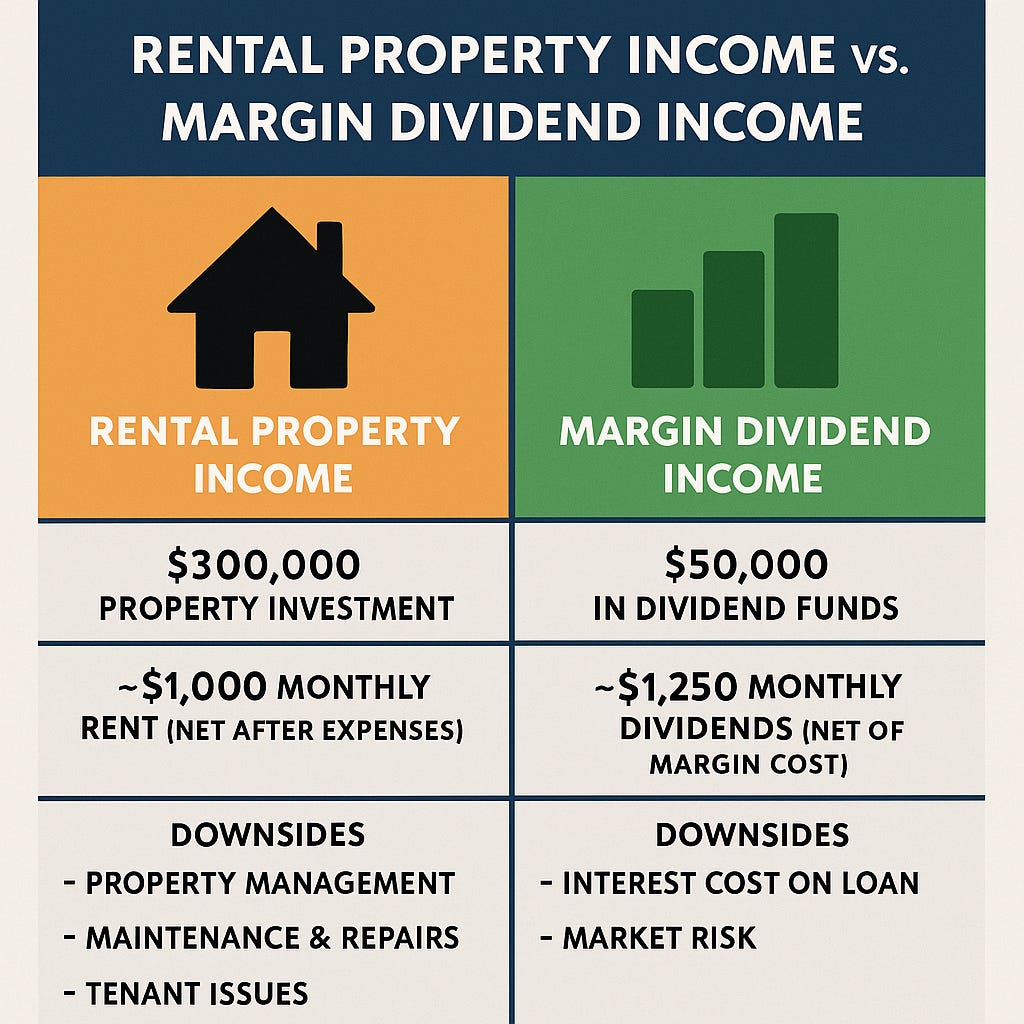

How This Cash Flow Rivals Rental Income Without the Headaches

One of the most common passive income dreams is real estate. People love the idea of owning a few rental properties, collecting monthly rent, and building long term wealth through appreciation.

But here is the reality most people do not talk about.

Rental income comes with a long list of challenges: property taxes, maintenance, repairs, vacancies, insurance, bad tenants, and sometimes legal headaches. Not to mention the massive capital needed for down payments, closing costs, and renovations.

Now compare that to a margin based dividend income strategy.

With $50,000 in high yield dividend funds paying 20 to 30%, it is possible to generate $10,000 to $15,000 in annual income or more if you carefully use margin to increase exposure. That is equal to or better than the net cash flow many landlords earn after all expenses are paid.

Plus, there is no roof to fix. No calls in the middle of the night. No tenants skipping rent. Just recurring cash flow that can be monitored and adjusted from a brokerage account. And unlike a rental property that pays monthly, some of these high yield ETFs pay weekly, offering even more control and flexibility over your income.

Of course, there are risks with both strategies. Real estate has leverage and market cycles. So do income funds. But when you run the math, dividend investing with margin can compete head to head with real estate cash flow with far less friction.

You do not need to wait years to buy your first property. You can start generating income from your portfolio right now.

Conclusion

Margin is not for everyone. But when used responsibly, it can unlock powerful income potential that rivals and in some cases exceeds more traditional paths like rental real estate. By borrowing at a lower rate to invest in high yield dividend assets, you create a spread that turns into real cash flow. That income can fund your lifestyle, speed up your financial goals, and create a compounding flywheel that builds over time. Like any tool, it demands respect, discipline, and risk awareness. But for income focused investors willing to think differently, this strategy can be a game changer.

This was super helpful and straightforward, thanks. Just to confirm are you doing this in a brokerage account or retirement account? And do you account for taxes in your math? So the example 15% spread is cut by margin fees and taxes (but still profitable)

Clear, clean cut breakdown, thank you for the explanation. Margin seems scary to someone new, who doesn’t know much about it.