You’re Broke Because Of A Rigged Game. Learn to Win & Stop Being A Victim

If You Don’t Own Assets, You’ll Always Be Owned

Let’s get one thing clear. You are not broke because you are lazy. If you’re reading this, you probably already take an above-average interest in your personal finances. You are broke because the entire financial system is designed to keep you that way. From the moment you are old enough to earn money, you are fed the same script.

Go to school.

Get a good job.

Save some money.

Avoid debt.

Live below your means.

Retire at 65 if you are lucky.

That script worked decades ago when a single income could buy a house, support a family, and build a future. But that world is gone. Today, prices rise faster than paychecks. Housing is unaffordable. Groceries cost more every month. Savings accounts pay you next to nothing. And if you try to play it safe, you get left behind.

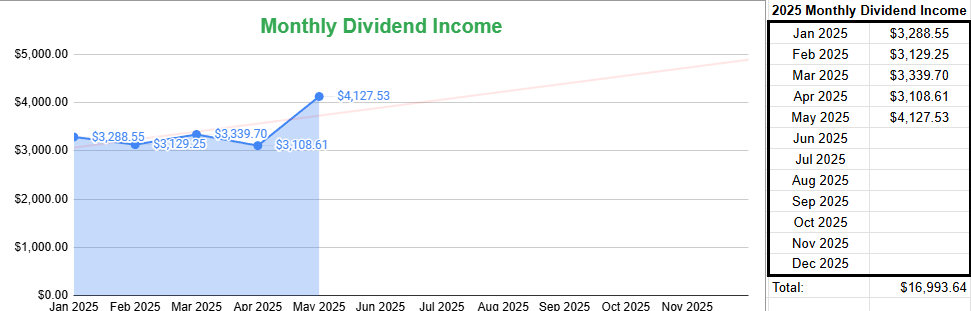

I’ve been able to offset these costs by building a second income stream of dividends. As you can see below, I collected a little over $4,000 in the month of May. I release monthly dividend reports for all readers.

This is the power of building income instead of just collecting paychecks.

I call it owning your time. Every time this portfolio grows, I buy a little more of it back. If you missed last month’s report, you can see that below.

May 2025 Dividend Report

When I graduated college, my first job paid me about $3,000 a month. I worked full-time, sat in traffic, juggled deadlines, and waited two weeks for each paycheck to hit.

The rules of the game have changed. But no one told you because the people who benefit from the system need you to keep playing the old game. They want you scared of investing. They want you dependent on a paycheck. They want you stuck in a cycle of survival while they build wealth in the background.

The truth is simple. Wealth is not built by saving what is left over after spending. It is built by owning assets that grow faster than inflation. It is built by creating income that works even when you do not. It is built by understanding how money actually moves in today’s world.

The Hidden Cost of Inflation

Inflation is not just some economic statistic for policymakers to debate. It is a slow, invisible force that quietly steals from you every single year. When the government injects more money into the economy, every dollar in your wallet becomes weaker. That might not sound dramatic, but the consequences are massive.

Most people do not feel the pain immediately. A few extra cents at the gas pump. A subtle price jump at the grocery store. Maybe your rent ticks up again, just like it did last year. But over time, this “normal” becomes destructive.

A 3% annual inflation rate might sound small. But compounded over time, it is devastating. After 10 years, your money loses over one fourth of its purchasing power. After 20 years, nearly half of it is gone. That means the $50,000 you have in savings today will only buy $27,500 worth of goods and services two decades from now.

And here is the worst part: your bank account is not helping you. Traditional savings accounts offer less than 1% in interest. That means your money is shrinking in value every day it just sits there.

If you do nothing, the outcome is already decided. Every year you wait, your dollars work less and your freedom costs more. The system is designed this way. Saving money feels responsible. But in today’s world, it is not enough. It is a trap dressed as safety.

The only way to fight back is to invest in assets that grow faster than inflation. Assets that produce income, that rise in value, and that compound over time. Because if your money is not growing, it is dying.

Why You Need to Own Assets

To escape the trap, you need to own things that benefit from inflation. That means stocks, real estate, businesses, and productive assets that grow in value over time.

If there’s one thing to take away from this article, it’s this: Assets turn inflation into your ally.

When inflation pushes prices higher, it also lifts the value of real assets. Stocks generate more revenue. Real estate commands higher rents. Businesses expand and raise prices to match demand. And the people who own those assets? They get richer.

That is why owning stocks, real estate, or income-producing businesses is not optional. It is essential. It is how you switch from being the one paying the price to being the one collecting it.

Think of it like this:

When you rent, inflation hurts you. When you own property, it helps you.

When you save in cash, inflation eats it. When you invest in stocks, inflation grows it.

When you work for money, you're capped. When you own money-making assets, you're scaled.

You do not need to be a genius. You do not need to time the market. You just need to stop giving away your time and money in exchange for things that lose value.

The longer you stay on the sidelines, the harder the climb becomes. Your goal is not to chase gains. Your goal is to own the system that produces them. That is how you stop surviving and start building.

What I Am Buying to Win

You do not need to pick the next big stock or time the market perfectly. You need to be consistent. Here are a few types of investments I am focusing on right now to benefit from inflation and interest rate dynamics:

Dividend Growth ETFs: Funds like SCHD and DGRO that own quality companies with rising cash flow and increasing dividends.

Why This Might Be the Greatest Dividend Growth ETF Ever Created

We are living in an era where inflation is no longer a background risk. It is front and center. While it has cooled from its 2022 peak, core inflation in the United States still hovers above the Federal Reserve’s two percent target, and many essential goods and services continue to rise in price year over year.

Real Asset Funds: Infrastructure and REIT funds like UTF or RNP that benefit from rising rates and rent growth.

Business Development Companies: BDCs like ARCC and MAIN that generate income by lending to private companies and adjusting rates as the market changes.

Option Income ETFs: Funds like GPIX and JEPQ that turn market volatility into high-yield cash flow. These funds can pay on a weekly or monthly basis.

I Analyzed 10 Option Income ETFs So You Don’t Have To

The explosion of option income ETFs has created a gold rush for yield-hungry investors. With the promise of monthly payouts, sky high yields, and hands off management, these funds sound like the perfect solution for anyone trying to build passive income.

These are not lottery tickets. They are cash machines. They pay me regardless of what the Fed does, how the economy feels, or whether stocks go up or down tomorrow.

📊 Tool: Track Your Progress

Want to keep track of what you're earning, how much your portfolio yields, and where to reinvest?

📥 Dividend Tracker Template – $5

Simple, powerful Google Sheet to track your holdings, income, yield-on-cost, reinvestment, and more.

📘 Full System: Go From $0 to $500/Month in Income

If you’re ready to build a scalable dividend income portfolio from scratch, with real structure, strategy, and support. You can start here:

🚀 The Dividend Income Blueprint – $25

My complete guide that shows how I built over $3,000/month in passive income using a three-layer dividend system, reinvestment strategy, and sustainable yield portfolio design.

It includes:

The strategy I use

Portfolio structure breakdown

Real examples + reinvestment tactics

Income planning + risk controls

Bonus: Checklist, glossary, & asset filters

Final Thoughts

The game is rigged. But only against people who never learn to play it. If you are tired of feeling like your efforts never move you forward, stop playing defense. Start buying assets that work for you while you sleep. Need guidance on where to start? Subscribe here as I continue to publish content and guides that can help you get your journey started in a way that matches your overall risk tolerance and comfort level.

Inflation is not going away. Prices will keep rising. Your rent, your groceries, your bills, all of it. The only way to get ahead is to own the kind of assets that rise with them.

Stop blaming the system. Learn it. Use it. Beat it.

Don’t be the grown ass adult that’s still complaining about the price of eggs.

Q2 Dividend Moves: What I’m Buying, Selling, and Watching Next

If you’ve been reading my posts for a while, you know I don’t just talk about dividend investing, I actually live it. Every move I make in my portfolio is based on real income, real risk, and a clear goal: to make work optional by building an income stream that pays me every single month.