These 5 Types of High Yield Dividend Stocks Can Pay You Monthly

Most investors only know 2 or 3 of these — do you know all 5?

The traditional advice used to work. Save diligently. Buy blue-chip stocks. Withdraw four percent a year and live comfortably in retirement. That used to be enough. But in today’s world, it is no longer a reliable strategy.

Interest rates are unstable. Inflation is sticky. The cost of living continues to rise while the average yield on a broad market index like the S&P 500 remains under two percent. Bonds do not offer the security they once did. And bank savings accounts barely pay more than zero after taxes and inflation.

If you are trying to build real cash flow from your investments, you’ll need income that shows up in your account monthly and helps cover actual bills.

The good news is that there is a solution. A growing universe of income-focused assets can help you generate consistent, reliable yield. Some pay five percent. Some pay over twelve percent. Many pay monthly and the last fund here pays weekly. And when blended together into a thoughtful portfolio, they can help you create financial independence much sooner than you might think.

In this guide, we will break down five categories of high-yield assets. Each one offers a different risk and reward profile. Some are slow and steady. Others are more aggressive but offer serious income potential. Together, they form a playbook you can use to create your own cash-producing portfolio.

Whether you are just starting to build wealth, preparing for retirement, or looking to replace your paycheck with passive income, this guide will give you the tools to start moving in the right direction.

1. Dividend ETFs: Simple, Scalable, and Liquid 💼

This one is easy and the one that you are most likely to be familiar with. Dividend ETFs are one of the easiest and most effective ways to start generating income from your investments. They offer broad exposure to dividend-paying companies and require zero active management. You buy them, hold them, and get paid. Easy.

These funds are ideal for both beginners and experienced investors who want predictable income with minimal effort. They can serve as a core building block in any income-focused portfolio. A dividend ETF holds a basket of companies that regularly pay dividends. Some focus on high yield, others on companies with a consistent record of raising their dividends, and some offer a blend of both. The ETF collects the dividends from the underlying stocks and passes that income along to you, usually every quarter or every month.

You are not relying on one company to deliver. You are relying on dozens or even hundreds of them. This diversification makes dividend ETFs more stable and lower risk than picking individual dividend stocks.

Examples of Popular Dividend ETFs

SCHD — Schwab U.S. Dividend Equity ETF

Focuses on high-quality companies with strong fundamentals and a history of dividend growth

Current yield: around 3.7%VYM — Vanguard High Dividend Yield ETF

Targets large-cap stocks with above-average dividend yields

Current yield: around 3.5%HDV — iShares Core High Dividend ETF

Screens for financially healthy, high-dividend companies

Current yield: around 4.2%

Benefits ✅

Diversification across sectors and companies

Steady income with low maintenance.

Low fees and high liquidity.

Great for reinvestment or withdrawals.

Suitable for both taxable and retirement accounts.

Considerations ⚠️

Yields are moderate compared to other high-income options.

Some ETFs may lean heavily into a few sectors.

Dividends can be reduced during downturns.

Less upside potential than growth-focused funds.

Portfolio Fit 📌

Dividend ETFs are an excellent foundation for any income strategy. They offer a clean, reliable way to collect passive income and reduce single-stock risk. Whether you are compounding through reinvestment or drawing income each month, these funds provide consistency and peace of mind.

Use them as your base layer. Once in place, you can build on them with higher-yield assets like REITs, BDCs, and option income ETFs to increase your overall cash flow.

Is DGRO Still One of the Best Dividend Growth ETFs in 2025?

Not all dividend ETFs are built for income. Some are built for growth and DGRO is one of the cleanest examples of that strategy.

2. REITs: Real Estate Without Being a Landlord 🏢

If you want to earn income from real estate but have no interest in managing properties or dealing with tenants, REITs are a smart alternative. A REIT, or Real Estate Investment Trust, is a company that owns income-producing properties and distributes most of the rental income to shareholders in the form of dividends.

REITs are required to pay out at least 90%of their taxable income, making them naturally suited for income investors.

How REITs Work

REITs collect rent from properties they own and pass that income to investors. These properties can range from apartment complexes and shopping centers to cell towers and data centers. Many REITs focus on a specific property type, which allows you to gain targeted exposure to parts of the real estate market that are difficult to access otherwise.

There are also REIT ETFs that provide exposure to a diversified basket of real estate companies, but many investors prefer individual REITs for their higher yields and monthly payouts.

Examples of Reliable REITs

Realty Income (O)

Known as "The Monthly Dividend Company," Realty Income owns over 13,000 commercial properties, mostly under long-term net leases.

Current yield: around 5.5%

Pays dividends monthlyW. P. Carey (WPC)

A globally diversified REIT that owns industrial, office, and retail properties across North America and Europe.

Current yield: around 6.5%Global X SuperDividend REIT ETF (SRET)

A high-yield REIT ETF offering international exposure with a current yield around 10%.

Note: This fund is more volatile and holds riskier names than traditional REITs

Benefits ✅

High yield, often in the 4% to 8% range

Passive real estate exposure with zero property management

Natural inflation protection since rents tend to rise over time

Many REITs pay monthly, which is ideal for income-focused investors

Considerations ⚠️

Sensitive to interest rate changes

May carry higher debt loads depending on the sector

Some sectors like office and retail can be cyclical or in long-term decline

Dividends are usually taxed as ordinary income unless held in tax-advantaged accounts

Portfolio Fit 📌

REITs add both diversification and cash flow to your income portfolio. They give you exposure to real assets, reduce your dependence on traditional equities, and help hedge against inflation. Monthly payers like Realty Income are especially useful for building consistent income that mimics a paycheck.

You can use REITs to complement your dividend ETFs and boost overall yield without sacrificing quality or liquidity.

Build Your Own Rental Empire With These 4 REITs

Imagine collecting rent checks every month from prime shopping centers, luxury casinos, grocery anchored retail strips, and iconic office buildings without ever buying a single property or managing a single tenant.

3. MLPs: Master Limited Partnerships 🛢️

Master Limited Partnerships, or MLPs, are income-focused investments most commonly found in the energy sector. They own and operate infrastructure like pipelines, storage tanks, and terminals that are essential to moving oil, natural gas, and petrochemicals across the country.

While energy stocks can be volatile, MLPs are often much more stable because they do not depend on commodity prices to make money. Instead, they charge fees for transportation and storage, which provides steady, toll-like income.

How MLPs Work

MLPs are structured as partnerships, not corporations. That means they do not pay corporate income tax. Instead, they pass most of their income directly to shareholders as distributions. In many cases, a large portion of these distributions is classified as return of capital, which defers taxes and lowers your cost basis over time.

Because of this structure, MLPs are best held in taxable accounts, not retirement accounts, to preserve their tax benefits and avoid potential complications with unrelated business taxable income.

Why Enterprise Products Partners (EPD) Stands Out

Enterprise Products Partners (EPD) is one of the largest and most reliable MLPs in the United States. It owns over 50,000 miles of pipelines and a network of storage, processing, and terminal assets that span coast to coast.

Here is why EPD is so compelling:

Current yield around 7%

25 consecutive years of distribution growth

Insider ownership is high, signaling strong alignment with investors

Very conservative balance sheet with a credit rating of BBB plus

Revenue is fee-based, not commodity-based, reducing exposure to oil and gas price swings

Often considered the blue-chip name of the MLP space

EPD has consistently rewarded long-term investors with a combination of high income, tax efficiency, and relative price stability.

Benefits ✅

High tax-advantaged income

Cash flows are supported by long-term contracts and infrastructure demand

Stable business model that performs well in different commodity environments

Attractive to income-focused investors seeking consistency

Considerations ⚠️

K-1 tax form adds complexity at tax time

Best held in a taxable account for full benefit

Energy sector exposure may not suit all investors

Not ideal for those looking for fast capital appreciation

Portfolio Fit 📌

EPD can serve as a powerful anchor in an income portfolio for those who want reliable, high-yield cash flow with tax advantages. While it is not as liquid as an ETF or as diversified as a fund, the stability of EPD’s operations makes it one of the few individual securities worth holding long-term for income.

It pairs well with more traditional dividend ETFs and REITs by offering a completely different source of income driven by physical infrastructure and energy demand.

4. BDCs: Business Development Companies That Pay You Back 💵

Business Development Companies, or BDCs, are a lesser-known but powerful asset class for income investors. These companies provide financing to small and mid-sized businesses that cannot easily access traditional bank loans. In return, BDCs receive high interest payments and equity stakes that they pass on to shareholders through dividends.

BDCs are legally required to distribute at least 90 percent of their taxable income to investors. As a result, many of them pay 8 to 12 percent annually, with several paying dividends monthly or quarterly.

How BDCs Work

BDCs operate like private lenders. They make loans that often have higher interest rates, to small businesses and sometimes invest in equity or convertible debt. Their portfolios often include dozens or even hundreds of companies across different industries.

The income BDCs collect from these loans is used to fund shareholder distributions. Many also benefit from rising interest rates because their loan portfolios are typically floating-rate, meaning they earn more as rates go up.

Examples of Quality BDCs

Main Street Capital (MAIN) - Widely considered a best-in-class BDC, MAIN is known for its conservative management, strong dividend coverage, and monthly payments.

Current yield: around 6.8%

Pays monthly

Ares Capital Corporation (ARCC) - One of the largest and most established BDCs in the market. ARCC has a strong track record of navigating different credit cycles.

Current yield: around 9.5%

Pays quarterlyTrinity Capital (TRIN) - A smaller but fast-growing BDC focused on venture debt and technology-related companies. Offers a higher yield with more risk.

Current yield: over 13 percent

Pays monthly

Benefits ✅

High income potential with yields commonly in the 8 to 12 percent range

Benefit from rising interest rates through floating-rate loan exposure

Diversified across dozens or hundreds of private companies

Many BDCs pay monthly, which helps with regular cash flow planning

Considerations ⚠️

BDCs are sensitive to credit risk and economic cycles

Leverage can magnify both gains and losses

Dividends are taxed as ordinary income unless held in tax-advantaged accounts

Smaller BDCs can be less liquid and more volatile

Portfolio Fit 📌

BDCs bring private credit exposure into your portfolio without the complexity of managing loans yourself. They are especially attractive to income-focused investors who want high yield and the ability to benefit from rising rates.

Use BDCs to increase your income yield above what dividend ETFs and REITs typically offer. They pair well with more stable assets, helping you balance risk while still collecting meaningful monthly or quarterly income.

How I’d Invest $10,000 To Eventually Earn $500/Month in Passive Income

Let’s be honest. Most people don’t get excited about dividends because they think you need a million dollar portfolio just to see meaningful income. The dividend payments in the beginning are relatively small. It becomes harder to stick with it when you don’t feel like you’re seeing progress. However, this changes over time when you stay committed.

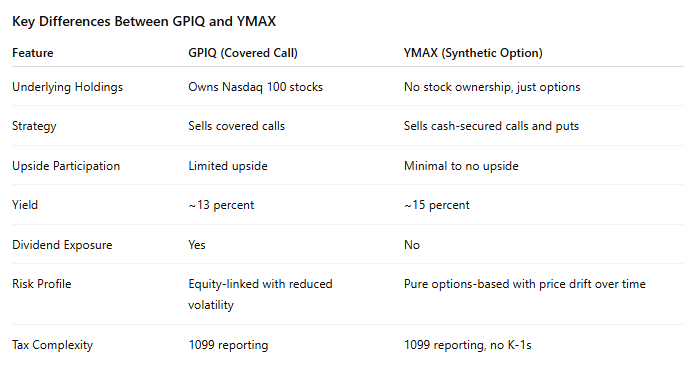

5. High-Yield Option ETFs: GPIQ vs YMAX 🧠

Option income ETFs have exploded in popularity because they offer what many investors are chasing — high, reliable monthly cash flow. But not all of them are built the same. Two common structures are covered call ETFs and synthetic option ETFs, and understanding the difference is key to using them wisely.

Let’s break it down by looking at two examples: GPIQ, a traditional covered call ETF, and YMAX, a synthetic option ETF.

GPIQ: Covered Call Strategy With Real Equity Exposure 🧾

GPIQ is a covered call ETF from Goldman Sachs that provides exposure to the Nasdaq 100. It holds the actual stocks in the index and then sells call options on those positions to generate additional income.

Owns Nasdaq 100 stocks directly

Sells call options against those holdings to boost yield

Still captures some upside from stock appreciation

Pays income monthly

Yield: around 13 percent

Offers real dividend exposure from the underlying stocks

This is a more conservative approach. Because GPIQ holds real stocks, it can still benefit if the market rises, although the upside is capped due to the call options. The result is a smoother ride than owning QQQ outright, but with much higher monthly income.

YMAX: Synthetic Options Strategy With No Stock Ownership 💡

YMAX, in contrast, is a synthetic option ETF. It does not own any stocks. Instead, it uses derivatives — usually cash-settled index options — to replicate exposure to the S&P 500 and generate income through a mix of call and put option sales.

Does not own S&P 500 stocks

Uses a synthetic collar strategy (selling calls and puts)

Designed to maximize option premium income

Pays income monthly

Yield: around 15 percent

No dividend exposure or equity upside

YMAX is built purely for yield. It delivers cash flow, but it will not grow in value alongside the stock market. The structure is optimized for flat or choppy markets where option premiums are high and equity returns are limited.

How to Use Each One 📌

Use GPIQ when you want consistent income plus partial market exposure with lower volatility. It is a good middle ground for income investors who still want to participate in the tech-heavy Nasdaq without the wild swings.

Use YMAX when you want maximum monthly cash flow and are less concerned with capital appreciation. It works well as a tactical yield booster or a temporary income position, but it should not be your core long-term holding.

Both GPIQ and YMAX have a place in an income strategy, but they serve different purposes. One offers real equity exposure with option overlays. The other is a synthetic tool built to maximize yield above all else.

Understanding how these funds generate income and what trade-offs they make is essential if you want to use them to your advantage.

7 Weekly Paying Dividend Stocks I Am Using to Boost My Income

One of the biggest mindset shifts I’ve made as an investor is this:

Conclusion: Build the Income Portfolio That Works for You

High yield investing is not about chasing the biggest number or taking reckless risks. It is about building a portfolio that produces steady, reliable income so your money works as hard as you do or harder.

Each of the five income categories we covered offers something unique. Dividend ETFs give you stability. REITs add real estate exposure. MLPs offer tax advantaged cash flow. BDCs bring in high yield private credit. Covered call ETFs like GPIQ provide enhanced yield from blue chip stocks. And synthetic option ETFs like YMAX maximize monthly income through a completely different engine.

You do not need to pick just one. In fact, the power comes from combining them thoughtfully. Build a mix that fits your risk tolerance, your lifestyle goals, and your income needs.

Because in the end, financial freedom is not just about growing a portfolio. It is about owning assets that pay you to keep living life on your terms, month after month.

Good to see that TRIN made your list! Another excellent post, Cain!